If you're a CFO at a growing e-commerce brand, "senior lender" can sound like legal jargon. It isn't. That lender often decides how much freedom your business has when inventory lands late, Amazon holds payouts, or demand spikes faster than planned.

I think about finance like structural engineering. If the senior layer is wrong, everything built on top of it gets weaker.

I care about this topic because I spent years in banking before I built Paperstack. I kept seeing strong consumer brands declined because the underwriting model was built for hard assets, not modern cash flow. Later, when we first built Paperstack as a CFO analytics tool, founders told us something very clearly: data alone doesn't move a business forward - capital does, when it's deployed with insight.

The market has changed fast. Lending logic has not. By 2025, online retail had grown to 16.4% of all U.S. retail sales. Still in 2023, only 37% of small U.S. employer firms applied for a loan or line of credit, and many were only asking for $100,000 or less. In 2024, 48% of applicants received less financing than requested.

Those numbers tell you a lot. Many operators have learned to ask for less, delay the process, or avoid it entirely. That gap matters when you are trying to fund inventory, marketing, and payroll on real timelines.

What a Senior Lender Really Controls

On paper, a senior lender is the lender with first priority in the capital stack. They usually hold the first lien. If the business gets into trouble, they are first in line to be repaid.

For a CFO, the more useful definition is much more practical. The senior lender usually controls the tone of the entire stack. They shape the covenants. They influence whether you can add another provider later. They affect how cash gets swept out of the business. They often decide whether your capital structure gives you room to operate or slowly boxes you in.

That is why I pay so much attention to structure. A senior lender is not just a source of capital. It is the party setting the rules around your liquidity.

This matters even more when people talk about venture debt. I hear founders discuss it as if it is some side layer sitting neatly beside the real senior facility. In many cases, venture debt is the senior facility. It often takes the first-lien position. So when you evaluate it, don't stop at the stated rate. Model the warrants. Model the covenants. Ask yourself a very simple question: are these covenants actually livable on a normal day, not just in the best month of the year?

Why the Old Senior-Lender Model Breaks in E-Commerce

During my banking career, I saw the same pattern again and again. One case that stayed with me was a DTC beverage brand doing more than $3 million in annual revenue. Their customers loved them. Margins were healthy. Cash flow was steady. They still got declined.

The bank saw outsourced manufacturing, so there were no hard assets to lean on. It saw seasonal revenue swings because summer demand was stronger. It saw marketing spend and treated it like pure expense. From a commerce lens, the company looked efficient. From a traditional risk model, it looked unstable.

That is the systemic lending gap I keep talking about. The underwriting model was not specifically built for CPG brands. It was built for factories, equipment, and balance sheets that look nothing like a modern omnichannel brand.

I see the same problem with inventory-on-hand covenants. I've seen this multiple times in seasonal businesses. The company sells through inventory during its busy season. Inventory on hand goes down. Then the borrowing base goes down too. But that is often the exact moment when the business needs working capital for fixed costs and the next production cycle.

What good is a senior facility if it tightens when you sell?

Banks may see warehouse inventory as collateral that makes them safer. For the brand, that same inventory can mean storage fees, aging product, and trapped cash. World Bank data shows smaller firms are 35% to 37% less likely to pledge collateral than larger firms. Asset-light businesses simply do not fit collateral-first lending well.

I also have a hard time with facilities that still come with personal guarantees, slow approvals, in-person friction, and rigid templates for businesses already doing real revenue online. If you are running a $5 million to $50 million brand, you need a lender that understands how internet businesses actually work.

Rule 1: Start with Cash Flow Quality Across the Whole Business

When I look at a business, I start with cash flow quality. I mean the predictability, timing, and sustainability of how money moves through the company. That is a far better measure of resilience than a static view of collateral.

If you run an omnichannel brand, you already know the issue is not only revenue. It is timing. Suppliers want deposits before goods ship. Amazon can delay payouts. Wholesale cash may land on net terms. Marketing spend goes out before the sale comes in. Growth isn't just about how much you sell, it's about when you sell it.

That is why I believe a senior lender should underwrite the whole business. DTC, marketplace, wholesale, retail distribution, and B2B all matter. I recently worked with a CPG brand that had revenue spread across Amazon, Shopify, and wholesale. Other providers wanted to underwrite one channel at a time or factor only the wholesale piece. The result would have been three or four different lenders, each with its own repayment schedule. That creates pressure. It does not remove it.

A whole-business view matters for risk too. If one provider only looks at Amazon and Amazon slows for a period, that lender may panic even if wholesale is growing and the total business is healthier. A lender underwriting the full company can understand how slowing one channel and scaling another can still be a very smart move overall.

This is also why I like seeing B2B channels in the mix. They often improve structural stability. I've seen brands sell in bulk to banks and law firms for corporate gifting. Those orders can come with larger quantities. If the product is personalized, the brand may even be able to request upfront security deposits because the inventory cannot easily be resold. And those gift recipients can later convert into direct customers. A senior lender that ignores that channel misses part of the P&L.

I also want lenders to read marketing correctly. Growing e-commerce brands often invest 15% to 25% of annual revenue into marketing. For many brands, that is one of the top three expense lines. Treating all of it as burn is lazy underwriting. I look at marketing spend as an investment engine. ROAS matters. Contribution margin matters. Cash conversion timing matters.

If you want a lender to understand that, back it with the data. Show 12, 24, or 36 months of historical performance if you have it. Break up that movement into numbers. If you are asking for $500,000, explain how that capital turns into inventory, ads, and top-line growth, and how fast the cash comes back.

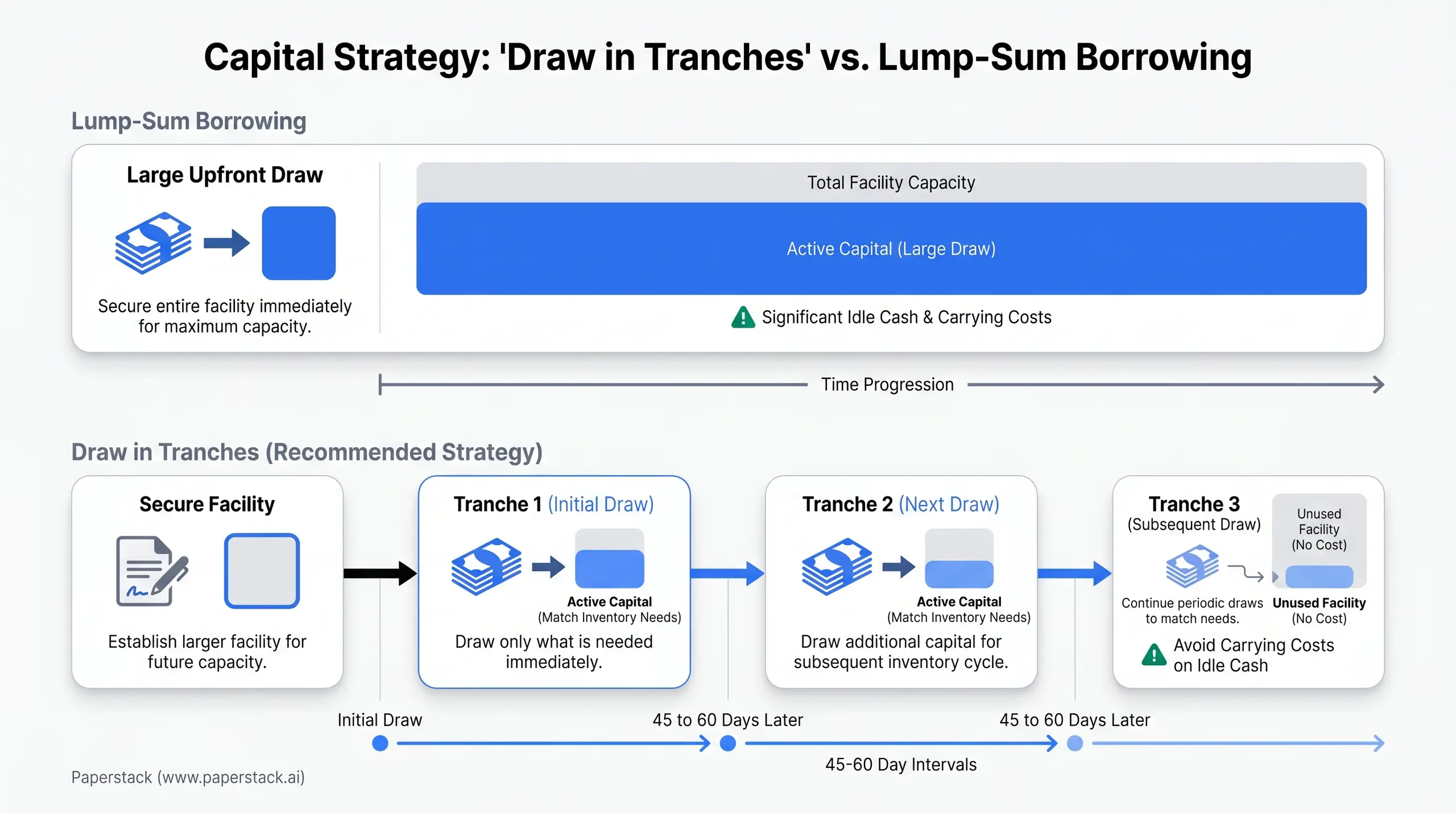

Rule 2: Secure Capacity, Then Draw in Tranches

One of the most common mistakes I see is taking the full approved amount upfront just because it is there. I understand the instinct. A large commitment feels safe. The math can become painful very quickly.

The moment you take capital upfront, you start paying for it. If the money sits in the bank account for the next two or three months, you are still carrying the cost of that capital. You are remitting toward a balance that has not generated you anything still. I often compare that instinct to maxing out a credit card for emotional comfort. The comfort is real. The economics are usually bad.

My view is simple. Secure the larger facility if the availability gives you peace of mind. Then draw what you need, when you need it. If you are not using that capital in the next 30 to 45 days, you should not be taking it upfront.

This idea shaped how we built Paperstack. I would much rather see a CFO have access to a larger revolving commitment and draw in smaller tranches every 45 to 60 days than carry the cost of idle cash. If the manufacturer needs a 30% deposit now, draw that portion now. Draw the rest when the goods actually leave the warehouse. That saves cost during the production lead time.

I have seen what happens when this discipline is missing. We helped an apparel brand that had taken a lump-sum facility and was remitting close to 25% of daily sales during slow months. Part of the problem was that the capital structure was too aggressive for their seasonality. We reworked it into 60-day tranches and refinanced the remaining balance over a longer period. That gave the business breathing room again.

I've seen the same issue in larger companies too. A scaling consumer brand doing over $20 million in revenue took excess capital "just in case." The daily remittances drained the bank balance and pushed the business into a cycle where it needed to borrow more money simply to relieve the pressure created by the first loan. That is exactly the trap I want CFOs to avoid.

Rule 3: Read the Structure Behind the Capital

A lot of offers look similar at first glance. Quick access. Non-dilutive. Growth-friendly. Then you dig into the structure behind non-dilutive capital, and the real story shows up.

I always tell CFOs to go past the headline rate. Ask for the all-in cost. Hidden fees are where many offers stop being attractive. Wire fees, origination fees, underwriting charges, admin fees, even fees for changing bank accounts can distort the economics. Terms are the keys.

Then get very specific on remittance. Are there minimum remittance thresholds that become painful in slower months? Is there a cap that protects the business if revenue spikes? At Paperstack, we use monthly caps because I do not believe brands should be penalized for growth. If a company suddenly grows fast, the lender should not drain liquidity faster than planned.

For brands with wholesale or Amazon timing, I also prefer repayment structures that reflect when cash actually lands. A percentage of bank deposits often makes more sense than a formula tied too tightly to front-end online sales. Cash flow quality matters. Timing matters.

You also need to understand how the lender treats your channels. Do they count wholesale revenue when the order is drafted, or when payment actually hits the account? Do they include all channels, or only the easiest one to plug into? Those details change forecasting accuracy.

Control over disbursement matters too. Some providers send funds to your bank account. Others pay suppliers or platforms on your behalf. That difference changes how much operational control you keep.

The same goes for consolidation. One senior lender can simplify a messy stack and lower cost. It can also create a severe operational vulnerability if that lender does not understand the uniqueness of your cash flow. A Q4-heavy business, a subscription brand with quarterly inflows, and a company with a fast-growing wholesale channel should not all be forced into the same covenant package.

Before you consolidate or layer on another provider, project how each facility will affect the cash flow of the business. If repayment sweeps, maturity dates, or covenants collide, one slowdown can create a domino effect on the rest of the stack.

Rule 4: Match the Capital Layer to the Job

I am very clear on this. Equity should be used for experimentation. New products, new channels, major hires, and international expansion belong in that bucket. Non-dilutive capital is far better for repeatable activities where you already know the economics, such as standard inventory orders and predictable advertising.

Consumer brands usually place inventory orders two or three times a year. If you keep using equity to fund those recurring cycles, the dilution adds up fast. In my view, the most expensive capital you can use for inventory or predictable marketing is equity.

There is an early-stage exception. If you are still trying to find a hero product, a mix of debt and equity can make sense. Once the business reaches several million dollars in revenue and has enough historical data, the case for non-dilutive capital becomes much stronger.

Venture debt sits in its own category, but it needs the same discipline. Deloitte estimates U.S. venture debt exceeded $30 billion a year from 2019 through 2022, fell to about $12 billion in 2023, and may rebound to roughly $14 billion to $16 billion in 2024. Availability will move with the market. The structure you sign stays with you.

So if you are evaluating venture debt, look beyond the price. Model the warrants. Understand the true cost of capital. Make sure the covenants are actually livable. And if you want to layer junior debt on top of senior debt, define the exact gap you are bridging and make sure the senior lender is comfortable with how that extra provider will affect cash flow.

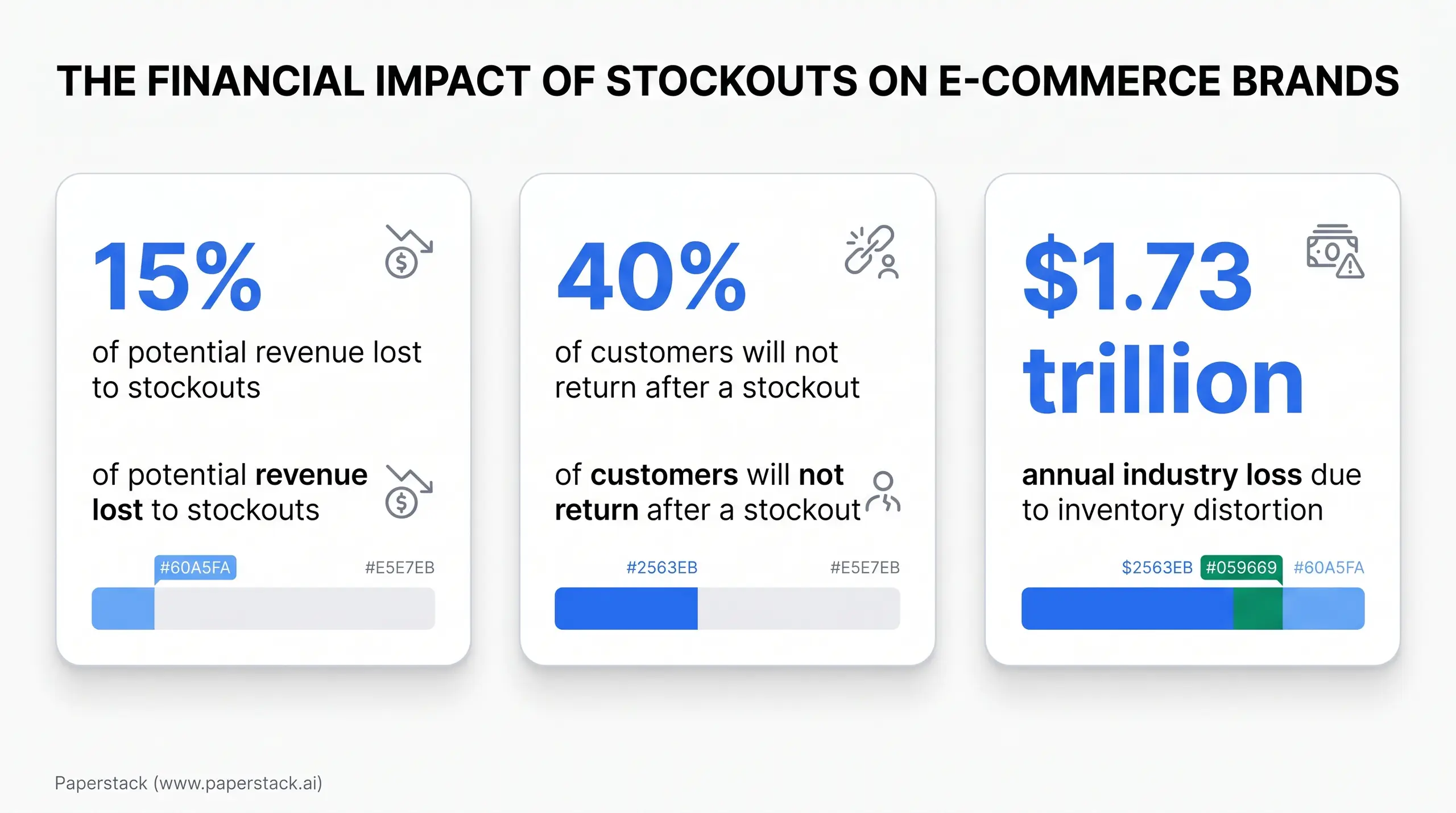

Rule 5: Treat Stockouts as a Capital-Stack Problem

I know stockouts can look exciting from the outside. Inside the business, they create pressure everywhere.

I have said many times that selling out is often a financial failure or operational failure. You drove the customer all the way to the point of purchase, and now there is nothing to buy. Then you have to rebuild the relationship with the customer, win them back, or keep them engaged until the product returns. That costs money.

The data supports that view. CPG brands lose about 15% of potential revenue to out-of-stock situations. Roughly 40% of customers will not return after a stockout. Another industry estimate puts losses from inventory distortion at $1.73 trillion annually.

I've seen this show up in very real ways. One wellness brand at roughly $5 million in revenue went viral and sold out on Amazon. Search ranking dropped. Visibility became harder to recover. Another wellness brand at around $10 million had a very efficient marketing agency that depleted inventory faster than expected. The team had to pause expansion into new channels just to preserve enough product for core DTC customers.

From the outside, that can look like a celebration. Inside the company, it is massive pressure. Your marketing team loses momentum. Fixed costs like warehouse rent keep running. Finance ends up scrambling for emergency purchase-order money. Then comes expensive air shipping, smaller production runs, or both. Earlier unit economics disappear fast.

There is one exception. Planned limited-edition drops can create useful scarcity. Your core products still need reliable availability. That part has to stay disciplined.

Rule 6: Demand Scenario Planning, Not Just Money

A senior lender should help you think through volatility, not just fund it. This is where my idea of unapologetic optimism comes in. Unapologetic optimism isn't about blind positivity - it's about discipline.

A recent survey found that 71% of finance leaders are putting more emphasis on scenario planning. Good. They should.

We do this often with brands at Paperstack. When one of our partners got hit by new import tariffs, we did not freeze. We ran conservative, most likely, and optimistic cases. We looked at unit economics, pricing flexibility, whether suppliers could split some of the cost, and what customer retention might look like if prices moved. Then we aligned a capital plan that could adjust as conditions changed.

That discipline gave the team room to keep ordering at scale and maintain supplier relationships while competitors hesitated. When the market stabilized, they were one of the few brands still fully stocked and able to capture market share.

The same logic applies when you get a port delay or an inventory gap. Sometimes the right move is to cut discounts and slow down marketing for a short period. That preserves inventory, protects margin, and gives you more room to absorb rush-restocking costs. A good senior lender should understand that move. They should not panic because one channel slows for the right reason.

What I Would Look for in a Senior Lender in 2026

If I were sitting in your seat, I would want a lender that understands the whole business and the uniqueness of my cash flow. I would want clear pricing, no surprises, and a structure that lets me draw capital as I need it instead of forcing me to pay for idle cash. I would want remittance caps that protect liquidity during strong months. I would want covenants that fit my business model. I would want continuity after funding, so I am not re-explaining the company every time conditions change.

Most of all, I would want alignment - not just access. The lender should understand how marketing, inventory, revenue timing, and channel mix work together. Capital should grow in rhythm with your brand.

Final Thought

I built Paperstack because I got tired of watching modern brands get pushed into outdated lending templates. My view has stayed the same. The next phase of commerce finance should feel more like a Stripe-style operating system for commerce capital than a one-off transaction.

A senior lender, at its best, gives you a durable foundation. It protects liquidity. It sharpens decision-making. It helps you act on the data you already have.

That is the bar for 2026. Capital starts working with your business, not against it.

Frequently Asked Questions

Why do scaling e-commerce brands often walk away with smaller senior facilities than their forecasts require?

Traditional underwriting penalizes asset-light models. Nationwide, 48% of applicants receive less financing than requested. Banks discount marketing spend and seasonal swings, forcing CFOs to accept inadequate capital that barely covers inventory cycles, limiting operational freedom.

When layering venture debt beneath a senior facility, what structural risks should a CFO model?

Venture debt is expected to hit $14 to $16 billion in 2024. Layering it requires strict intercreditor agreements. You must model the warrants and ensure maturity dates never collide with your senior facility. If repayment sweeps clash, one slowdown collapses your liquidity structure.

How can an asset-light D2C brand negotiate a strong borrowing base without hard collateral?

Shift the conversation from static inventory to cash flow quality. Data shows small firms are 35% to 37% less likely to pledge collateral. Present historical data showing exact cash conversion cycles. Prove how fast ad spend turns into revenue to replace hard assets with predictable velocity.

What specific forecasting data convinces a modern senior lender to underwrite an omnichannel strategy?

Demonstrate disciplined volatility management. Today, 71% of finance leaders emphasize scenario planning. Bring conservative, baseline, and optimistic models factoring in supplier delays and ROAS shifts. Showing how unit economics absorb shocks proves stability far better than aggressive top-line revenue forecasts.

Should mid-market e-commerce CFOs still rely on large traditional banks for senior credit facilities?

While 44% of loan applicants still approach big banks, rigid criteria rarely fit e-commerce cash flows. Large institutions demand personal guarantees and slow approvals. You need a capital partner offering tech-enabled underwriting that dynamically aligns remittance obligations with real-time revenue.