Most ecommerce lending facilities break long before default. They break in the structure.

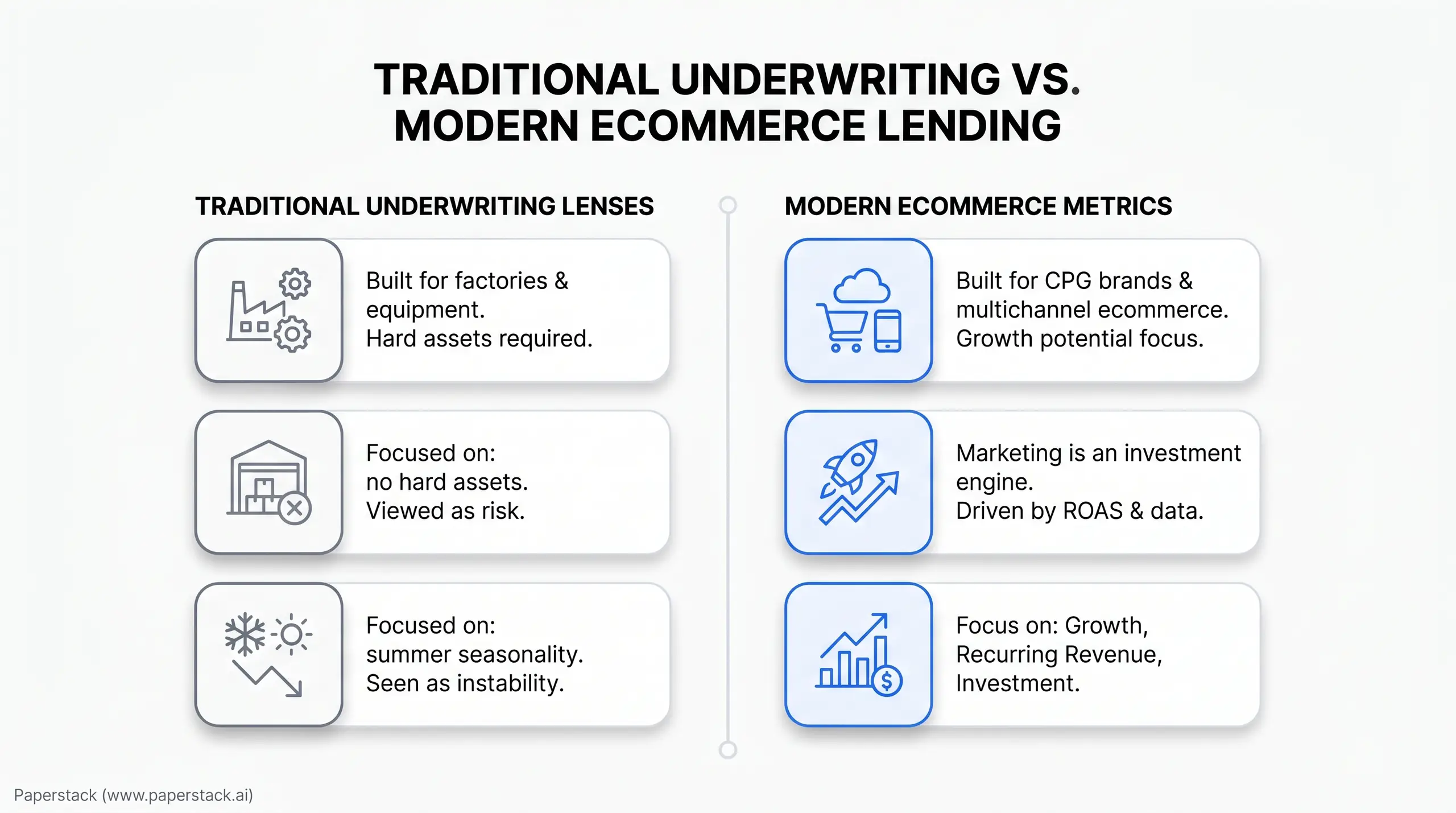

I learned that first in banking. I kept seeing strong consumer brands get declined for reasons that had very little to do with the health of the business. One DTC beverage brand was doing more than $3 million in annual revenue. Customers loved the product. Margins were healthy. Cash flow was steady. The bank focused on three things: no hard assets, summer seasonality, and marketing spend that looked like an expense. The business was declined.

That was one of the clearest systemic lending gaps I saw. The underwriting model was built for factories and equipment. It was not built for CPG brands or multichannel ecommerce. From a commerce lens, that brand was operating efficiently. From an outdated lending lens, it looked unstable.

I saw the same lesson again when we built Paperstack. We started as a CFO analytics platform. Founders told us the dashboards were useful, but they needed capital to act on the insights. That changed our business. It also sharpened my view on lending. Data alone doesn't move a business forward. Capital does, when it's deployed with insight.

Why This Matters Even More in 2026

CFOs have more financing options now. That sounds good. In practice, it also means more room to make an expensive mistake.

The funding gap is still very real. A 2024 Fed survey found that only 41% of applicants received all the financing they sought, 36% received some, and 24% received none. In the same survey, 41% of denied firms cited too much debt. That number matters. It tells you many businesses are not just struggling to access capital. They are already carrying the wrong kind of capital.

You can see that stress in how businesses fund themselves. An NBER report found that 55% of small firms used business credit cards in the past year, while only 27% used lines of credit and 26% used traditional loans. I understand why. The same study found that 61% cited ease of access and repayment flexibility. But a credit card is not a capital strategy for a brand placing inventory orders two or three times a year and spending heavily on ads.

This is also why many ecommerce brands outgrow banks quickly. Traditional bank loans for CPG still often come with personal guarantees, in-person meetings, and long approval cycles. That friction is hard enough. The bigger issue is the model behind it.

Start with Cash Flow Quality

When I evaluate a lending facility, I start with cash flow quality. I care about predictability. I care about timing. I care about sustainability. I want to know how money leaves the business, how it comes back, and how stable that pattern is across channels.

This is where many lenders still get ecommerce wrong. They treat marketing spend as an operating expense and stop there. In a healthy growth brand, marketing is an investment engine. It can be one of the top three expense categories alongside inventory and shipping. I regularly see brands allocating 15% to 25% of revenue to it. If a lender cannot understand how that spend converts, they are missing a huge part of the business.

So if you are the CFO telling the story to a lender, back it with the data. Show it with the numbers. Show how much revenue has historically gone to advertising. Show which channels you used. Show how ROAS moved as spend increased. Show whether the sales stayed profitable after product cost, shipping, discounts, and financing.

You also need to answer one hard question early. Does your business need profitability on the first purchase, or does it work because of long-term LTV? That answer shapes the right marketing budget. It also shapes the right lending structure. I have seen brands stay profitable at 2x or 2.5x ROAS, depending on AOV and subscription behavior. Others need more room.

Size the Facility Around the Operating Rhythm

I think about finance as structural engineering. Capital, inventory, and marketing have to move together. If one gets ahead of the others, the business gets squeezed.

Growth isn't just about how much you sell. It's about when you sell it. That means your facility needs to reflect the real timing of your business. Start with the supplier deposit schedule. Then add production lead times, freight, customs, Amazon payout timing, wholesale receivables, and the point when marketing actually begins to convert. Break that movement into numbers.

I also want finance and marketing much closer together than they usually are. If your team is scaling ad spend without understanding the efficiency curve, you are creating risk. If your finance team is building a lending facility without understanding the marketing calendar, you are borrowing blind. At certain stages, the smartest move is to slow customer acquisition and focus on upselling your base, raising AOV, and expanding LTV. More spend is not always the better answer.

Draw in Tranches, Not for Comfort

One of the biggest mistakes I see is emotional. Founders and operators feel tempted to get all the money upfront just to give themselves a sense of security. I understand the instinct. I still think it is dangerous.

The moment you take capital upfront, you start paying for it. If the cash is sitting in your account for the next 30 to 45 days, you are remitting toward that balance while the money has not generated you anything. What do you do with the cash, and if you do nothing, how much does it cost your business to keep it in the bank account? That is the question.

A better structure is a committed facility with tranche draws. On a standard 90-day manufacturing cycle, I would usually line it up in stages. First, fund the inventory deposit. Then draw again for the final payment when goods ship or arrive. Then draw marketing capital when the inventory is actually ready to sell. Why would you draw ad dollars 60 days before the goods arrive? You would just be carrying the cost of that capital.

At Paperstack, this is exactly why we built a revolving facility instead of a small one-off advance. We prefer committed capacity and smaller draws as needed. In many cases, that means draws every 45 to 60 days. It gives the CFO peace of mind without forcing the business to pay for all the cost of capital upfront while it is not using it.

I have seen what happens when brands do the opposite. One apparel brand became unprofitable in slower months because it was remitting close to 25% of daily sales on a lump-sum loan that had not been fully put to work. We refinanced that balance, moved the business into 60-day tranches, and stretched the payback period so the remittance would not be as severe. I have also seen a consumer brand generating over $20 million take extra capital "just in case." The daily remittances drained the bank account and pushed the company into a cycle of needing more money to cover the pressure created by the original facility.

Terms Matter More Than the Headline Rate

This is where many CFOs get frustrated. Two offers can look similar on paper and behave very differently once the business is running.

I always tell teams to go past the rate card. Ask about the actual total cost of capital. Ask about origination fees, underwriting charges, wire fees, admin fees, and fees for changing bank accounts. Hidden costs are common. Terms are the keys.

Then get very specific on repayment. Is remittance based on online sales or daily bank deposits? For Amazon and wholesale businesses, I often prefer deposit-based remittance because it better reflects when cash has actually landed. Ask whether there is a minimum payment during slow months. Ask whether there is a cap during strong months. You do not want a structure that takes a full month's remittance in the first week because sales came in fast.

This matters even more for fast-growing brands. We work with companies that hit double- and triple-digit growth. I do not think a lender should penalize them for growth by draining liquidity faster than planned. Monthly caps protect the business and make forecasting cleaner.

You also need clarity on what revenue counts and when. If wholesale is part of the business, is the lender giving you credit when a draft order is created in Shopify, or only when payment reaches your bank account? That detail changes your cash forecast. It also changes your real borrowing capacity.

And do not forget control. Some providers wire the money to your business. Others pay suppliers or ad platforms on your behalf. That changes flexibility. It changes speed. It changes how much operational control you still have.

Support matters too. I prefer continuity. At Paperstack, the person who originates the facility stays close to the relationship after funding. CFOs should expect that level of context from any capital partner. You should not have to re-explain your business every time something changes.

Underwrite the Whole Business

I feel strongly about this. A multichannel brand should be underwritten as a whole business.

I recently worked with a CPG brand that had strong repeat customers, good margins, and steady month-over-month growth. The real issue was timing. The company had to pay suppliers about 60 days before receiving inventory, and then wait for Amazon payouts to come in. Revenue was spread across Amazon, Shopify, and wholesale. Other capital providers wanted to finance only one piece of that picture. That would have left the team with three or four lenders, three or four repayment schedules, and a lot more stress.

We underwrote the total performance of the business. That gave the brand one clear source of capital. It also gave the team room to say yes to strategic retail partnerships without starving DTC or cutting marketing to conserve cash. That is what alignment looks like.

One lender can absolutely simplify the stack. It only helps if that lender understands the full business. If they miss your seasonality, your wholesale timing, or your quarterly payout pattern, the simplification becomes a new source of risk. From the outside, a business with several capital providers might look riskier than it really is. The bigger risk often sits inside the structure.

Give Proper Credit to B2B Channels

I also like facilities that give real credit to B2B. Those channels can make a brand structurally stronger.

I have seen brands sell products in bulk to banks and law firms for corporate gifting. That created larger order quantities and better stability. It also worked like funded customer acquisition, because some gift recipients later became direct customers. In practical terms, you are reaching more consumers while spending zero dollars on ads.

In cases like that, I would encourage the brand to position the product as a gifting opportunity, offer personalization like logos, and ask for a deposit. Customized inventory gives you a strong reason to request upfront security. Then use a land-and-expand approach. One good contract inside an institution can lead to referrals across offices and cities.

I also like when brands deliberately diversify revenue to minimize seasonality. I have seen an accessory brand lean into retail, wholesale, and B2B because relying on one big Q4 moment created too much risk. I am ultimately not a huge fan of betting 70% or 80% of annual revenue in a month or two.

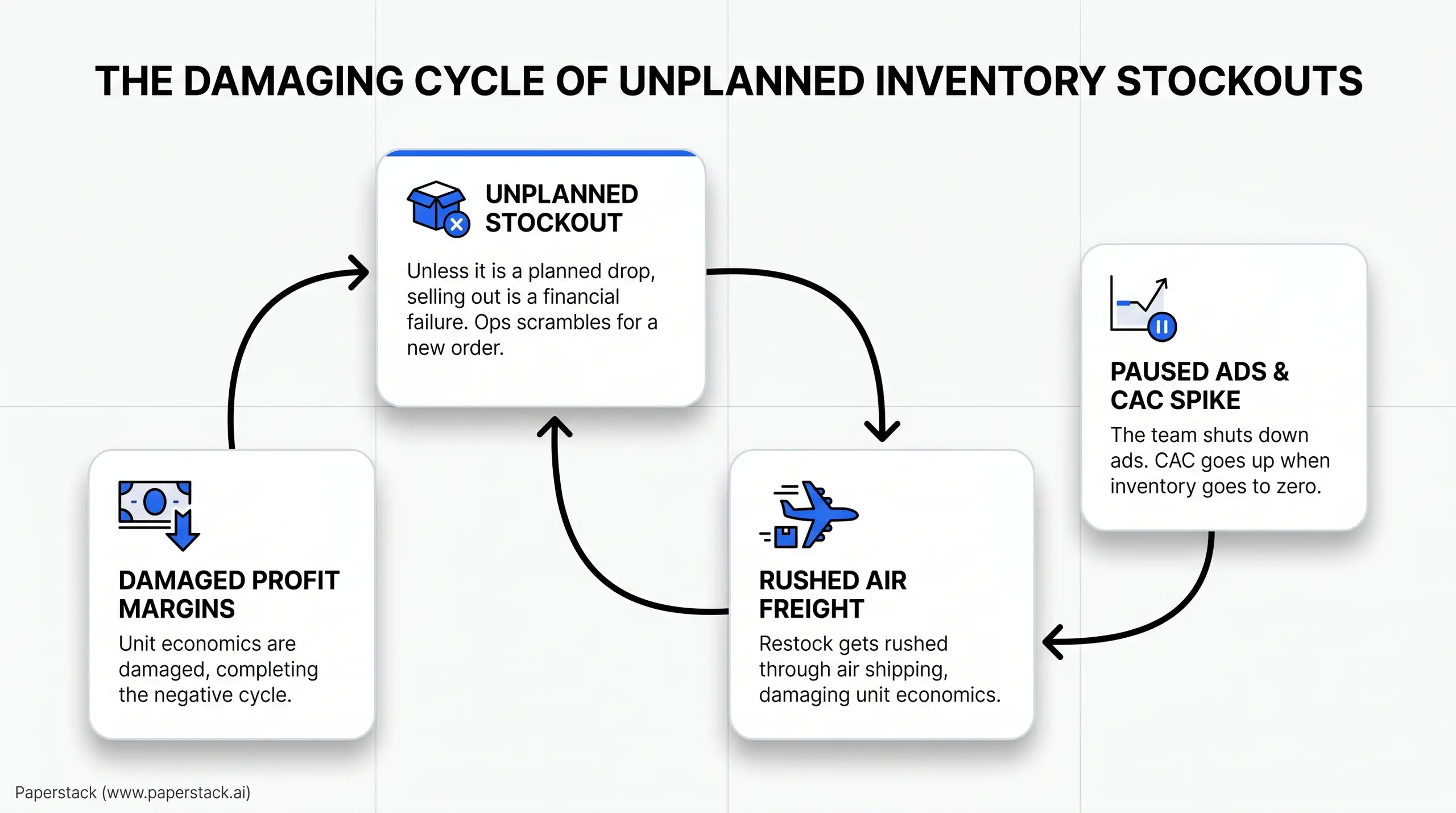

Treat Stockouts as Financing Failures

Many teams still celebrate selling out. I do not.

Unless it is a planned limited-edition drop, selling out is a financial failure or operational failure. It creates more stress than value. The team has to shut down ads that were working. Operations starts scrambling for a new order. The restock often gets rushed through smaller production runs or air shipping, which damages unit economics. If Amazon is a major channel, visibility can drop fast.

I have seen that very clearly. A wellness brand at roughly $5 million in revenue went viral and sold out on Amazon. The stockout hurt its search ranking and made it hard to regain visibility. Another wellness brand, closer to $10 million, had a very efficient marketing agency. Inventory moved faster than expected. The company had to pause expansion into new channels and reserve what was left for its core DTC customers.

From the outside, it might look like a celebration. From the inside, it is a massive pressure operationally for the team. You still have warehouse rent. You still have payroll. You still have fixed costs. At the same time, you now have to rebuild the relationship with the customer, win them back, or keep them engaged until the product arrives. CAC goes up right when your inventory has gone to zero.

Seasonality makes this even sharper. I often use a snack brand around $10 million in revenue as a simple example. The business faced a summer cash crunch while still needing to prepare for stronger periods later in the year. A rigid fixed-payment facility would have created pressure exactly when the business needed room. A revenue-based structure, or a stronger B2B channel, can help offset that seasonality.

I also challenge the reflex to wait until Black Friday to launch promotions. Start earlier. Avoid the worst CAC spike. Protect profitability before the market gets expensive.

Stress-Test the Facility Before the Market Does It for You

Unapologetic optimism isn't about blind positivity. It is about discipline.

One of our brand partners was hit by new import tariffs that changed landed costs almost overnight. Most finance leaders in that moment start freezing inventory and cutting marketing. I prefer to slow down, model the cases, and create options. We ran conservative, likely, and optimistic scenarios. We adjusted unit economics. We looked at whether the supplier could split part of the cost. We modeled what customer retention might look like if prices increased. We reviewed fixed costs and cash needs under each path.

That discipline matters because volatility is normal. By April 2022, 78% of U.S. small businesses reported price increases on inputs or supplies. You cannot build a facility as if shocks are rare. You should assume they will happen and decide in advance which levers you will pull.

Sometimes the easiest first move is operational. Raise the free shipping threshold from $100 to $150 or $200. Give loyal customers advance notice that prices may go up in two or three months. That can create a short-term spike in demand and give you cash to absorb the change. If you have built strong social capital with suppliers, ask them to share part of the cost.

If a port strike or supply delay hits, slow down promotions so you can preserve inventory and keep the sales you do make more profitable. That feels counterintuitive to some teams. I still believe it is the right move. You need room to absorb the emergency freight or rush restock if it comes.

For larger brands, I also like to see manufacturing diversification. If you are already at seven or eight figures, spreading production across countries or continents can protect the business from a single tariff shock or delay.

Match the Capital Type to the Job

I have a simple view on this. Equity is for experimentation. Non-dilutive capital is for repeatable activities.

If you are still early and trying to find the hero product, a mix of debt and equity can make sense. Once the brand reaches several million in revenue, and certainly once it is above $10 million with enough history, standard inventory and proven advertising should move to non-dilutive structures. You now have enough data to tell the story to a lender and back it with historical performance.

If you are presenting that shift to a board, keep it simple. Show 12, 24, or 36 months of performance. Show how inventory orders recur. Show how marketing has performed over time. Then break down how a specific capital injection will convert into top-line revenue. The board needs to see the math, not just the ambition.

Asset-based lending can work well for wholesale- and retail-heavy brands because inventory and receivables are meaningful assets there. Venture debt can also be useful, especially right after an equity round. But you need to review the true cost of capital carefully. Look at the warrants. Look at the covenants. Make sure they are actually livable for your business model. And remember that venture debt usually sits as the senior facility with a first-lien position. Treat it that way in your stack planning.

Traditional inventory-on-hand covenants can create a different problem. They push seasonal brands to hold product longer than they should, pay storage costs, and watch the borrowing base shrink right when they need working capital for the next order. That is bad structure.

The Questions I Would Ask Before Signing

Before you sign anything, ask direct questions. What is the true all-in cost after every fee? Which sales channels are included in underwriting? How is wholesale recognized? Are repayments tied to bank deposits or online sales? Is there a monthly cap?

Then ask the harder ones. If I draw this money and do nothing with it for 45 days, how much does it cost my business to keep it sitting in the account? Who owns the relationship after funding? And if I already have senior or junior debt in the stack, how will this new facility affect the rest of my cash flow?

You want alignment, not just access. You want a partner who understands the uniqueness of your cash flow and can structure the growth capital in a way that empowers the brand.

Final Thought

I built Paperstack because I saw too many good businesses getting pushed into outdated lending structures. In 2026, the best ecommerce lending facility will do a few things very well. It will reflect the full performance of the business. It will draw in rhythm with inventory and marketing. It will protect daily liquidity. It will give you room to grow without forcing you to pay for idle cash.

That is the future I believe in. A lending facility should feel like part of your financial operating system. It should grow in rhythm with your brand. When the structure is right, capital starts working with your business, not against it.

Frequently Asked Questions

What happens if our balance sheet is already burdened with rigid, high-interest debt?

You are not alone. A 2024 Fed survey found 41% of denied firms cited too much existing debt. We routinely refinance rigid lump-sum loans into flexible, tranche-based ecommerce lending structures. This immediately improves your cash flow coverage ratio by aligning repayment obligations directly with your actual multichannel sales velocity.

Are corporate credit cards sufficient for managing our working capital cycles?

No. While a 2025 NBER report notes 55% of small firms use corporate credit cards for quick access, they are not a scalable capital strategy. For mid-market brands spending heavily on inventory and ads, credit cards create dangerous repayment friction. You need a dedicated ecommerce lending facility structured around your exact operating rhythm.

How do rising input costs impact the sizing of our ecommerce lending facility?

Inflation directly shrinks purchasing power. By April 2022, 78% of small businesses faced price increases on supplies. Your ecommerce lending facility must account for margin compression. We size committed capacity to absorb emergency freight or higher landed costs, ensuring you maintain daily liquidity without ever pausing profitable marketing spend.

What internal financial controls do modern alternative lenders require during underwriting?

We look far beyond basic P&L statements. Modern ecommerce lending requires granular visibility into unit economics, channel-specific ROAS, and accurate inventory turnover rates. Your internal controls must seamlessly sync Shopify, Amazon, and wholesale data. If your forecasting clearly bridges marketing spend and delayed payouts, you will secure significantly better capital terms.

How do traditional financial covenants typically fail scaling multichannel operations?

Traditional covenants restrict working capital exactly when you need it most. Outdated inventory requirements force seasonal brands to pay unnecessary storage costs while shrinking their borrowing base. A proper ecommerce lending facility removes these rigid constraints, focusing entirely on cash flow predictability and realistic tranche draws aligned with your actual production cycles.