If you are a CFO, your first instinct is probably to ask one thing: what is the APR?

Fair. You need a clean way to compare offers. I would ask the same question.

But in e-commerce, that question can send you in the wrong direction. A lower APR can still hurt your business more. A higher implied APR can still be the better decision if the structure fits your cash flow, your inventory cycle, and your seasonality.

I care about this because I saw the gap up close in banking. I watched a DTC beverage brand doing over $3 million in annual revenue get declined for financing. The bank saw no hard assets, seasonal swings, and marketing spend showing up as expense. I saw healthy margins, steady cash flow, and strong demand. The underwriting model was not specifically built for CPG brands. That was one of the clearest systemic lending gaps that pushed me to build Paperstack.

The pressure on operators today is real. The Federal Reserve Small Business Credit Survey found that only about 41% of small-business applicants got the full financing they asked for in 2024, while 36% got only part of the amount and 24% got nothing. In that same report, 75% said rising input costs were their top financial challenge, and 51% reported uneven cash flows. On top of that, only 17% of firms reported a loan with an APR below 5% at the start of 2024.

So yes, finance teams are rate-sensitive. They should be. But they cannot stop there.

What APR Tells You - and What It Misses

APR Is Annual Math. Your Cash Cycle Is Not.

APR is useful. I still calculate it. If I am comparing standard debt products with similar fees and similar payment schedules, APR helps.

But revenue-based financing behaves differently. In RBF, the fee and the repayment rhythm are two separate levers. The fee tells you the price. The remittance tells you how hard the capital will pull on your cash flow while you are paying it back.

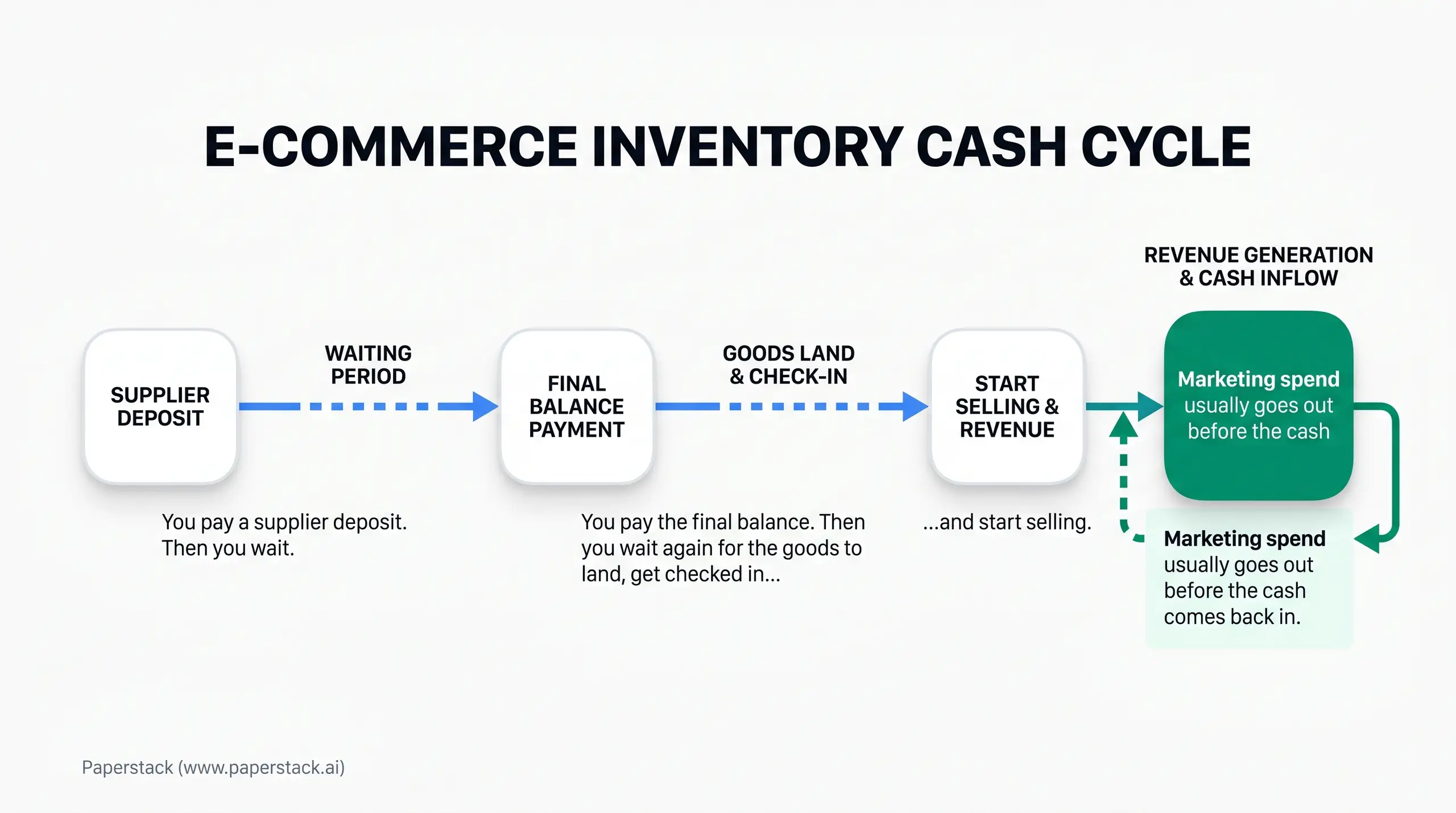

For an e-commerce brand, timing drives everything. You pay a supplier deposit. Then you wait. You pay the final balance. Then you wait again for the goods to land, get checked in, and start selling. Amazon payouts can lag. Wholesale might sit on Net 30 or Net 60. Marketing spend usually goes out before the cash comes back in. Growth isn't just about how much you sell, it's about when you sell it.

This is where APR can distort the picture. A flat fee on a short, profitable inventory cycle can look expensive when you stretch it across a year. The dollar fee did not change. The calendar changed. On the other side, a lower-APR facility with fixed payments can create much more stress in a slow month because the cash still leaves the business whether sales came in or not.

I have seen this with seasonal brands again and again. An approximately $10 million snack brand can have a very real summer cash crunch even if the full year looks healthy. A rigid payment schedule ignores that reality. A revenue-based structure can handle it better because the remittance moves with actual sales.

APR Says Nothing About Fit or Control

APR also tells you nothing about how usable the capital actually is.

One provider may send funds to your bank account. Another may pay your supplier directly. One may let you use capital across inventory, marketing, and operating expenses. Another may limit you to one bucket. One may let you draw as needed. Another may push you to take the full amount on day one.

Same headline rate? Maybe. Same value? Not even close.

That is why I keep coming back to one thing: understand the uniqueness of your cash flow. APR is one number. Your business is a system.

Why Flat Fees Can Work so Well for Inventory Cycles

Knowing the True Dollar Cost Upfront

A flat fee gives you something many CFOs care about more than people admit. Clarity.

If you draw $100,000 on a facility with a 10% flat fee, you know the total payback is $110,000. That matters. Now you can take that $10,000 and build it straight into the order. Add production, freight, duties, storage, returns, and expected markdowns. Then ask a simple question: does this order still make money?

That is why I often like flat-fee structures for predictable inventory purchases. Knowing a true dollar cost upfront lets you decide quickly and rationally. You are not trying to reverse-engineer a moving rate while a factory deposit is due.

This is especially helpful for scaling brands. If you know the inventory flip is repeatable, the fee becomes part of the operating math. You can see whether the margin still holds before you commit.

Use Non-Dilutive Capital for Repeatable Moves

This is also why I think CFOs need to separate predictable spending from experimental spending.

When we first started Paperstack, we actually began as a CFO analytics platform. Founders kept telling us the same thing. Better visibility was useful, but it did not solve the inventory payment sitting in front of them. Data alone doesn't move a business forward - capital does, when it's deployed with insight.

I feel very comfortable using non-dilutive capital for repeatable activities where you know the cost and can model the return. Inventory is a great example. Predictable marketing can be too, if the business has enough history. In my experience, growing e-commerce brands often invest 15% to 25% of annual revenue into marketing. That is one of the biggest expense categories in the business. I do not view that as random burn. I view it as an investment engine when the business can prove the return.

But if the capital is for a brand-new product, a new channel, or something still unproven, I get more cautious. The most expensive capital that you can use for inventory or predictable marketing is equity. Reserve equity for experiments. Use non-dilutive capital for the recurring moves once the data is there.

The Fee Is One Number. Remittance Is Another.

This is where many teams miss the real risk.

The flat fee tells you what the capital costs. The remittance structure tells you how manageable the payback will feel in real life. Two offers can carry similar fees and still behave completely differently once they hit your bank account.

I always ask what happens in the slow months. Is there a hard minimum remittance that keeps draining cash when revenue dips? Is there a cap that protects the business in a breakout month? How is wholesale revenue counted? When the draft order is created, or when the cash actually lands?

These details matter more than people think. I have seen structures that looked fine on paper and then forced a brand to pay a full month's remittance very early because the setup was too aggressive. That puts additional stress on cash flow and can create a domino effect across payroll, freight, and the next purchase order.

At Paperstack, we use monthly caps because I do not think brands should be penalized for growth. We do not penalize them for growth. If a business has a huge month, I still want it to have the liquidity to operate.

This flexibility matters most when demand gets messy. If sales go up, the business remits more. If sales go down, it does not have to stress too much. It remits the portion of what it actually generated. That is one of the biggest reasons I advocate for revenue-based financing during uncertain periods.

The Hidden Traps Behind a Low Headline APR

Cheap Can Get Expensive Very Quickly

Terms are the keys.

I have seen offers with minimum cash balance requirements. That sounds minor until you think about what it actually does. Now your cash is sitting in the bank account because the lender wants it there. It cannot buy inventory. It cannot fund marketing. You are carrying the cost of that capital while the money is not doing anything for the business.

I have also seen growth KPIs, admin fees, wire fees, and fees for changing bank accounts. Some offers allow only inventory. Some allow only marketing. Some require invoice submission every time you need funding. Some providers send the money to your supplier instead of to you. That affects operational control in a very real way.

A low APR with restrictive terms can be more expensive than a transparent flat fee. You end up paying for the capital before it is useful, or you lose the freedom to move cash where the business actually needs it.

One-Channel Underwriting Creates Blind Spots

This gets even more dangerous when a multi-channel brand uses multiple lenders.

We worked with a CPG brand that had revenue spread across Amazon, Shopify, and wholesale. Other capital providers would underwrite only one channel, or factor only the wholesale orders. The result was three or four different lenders, each with its own repayment schedule. From the outside, that might look like more access. Inside the business, it creates more pressure, more forecasting problems, and more operational risk.

We underwrote the whole business. That changed the conversation. The brand could say yes to strategic retail partnerships and still protect its DTC channel without cutting marketing just to preserve cash.

This matters because a one-channel lender can panic over the wrong signal. If Shopify is only 30% of your revenue and Shopify slows down for a month, that does not mean the whole company is in trouble. A provider underwriting the whole business will understand how slowing one channel or scaling another can still have a net positive effect overall.

The broader market is pushing more companies into this maze. C2FO's 2024 working capital survey found that 54% of business leaders saw high interest rates as the biggest barrier to funding and 42% expected rising rates to hurt growth. In that same survey, about 60% of companies said longer customer payment terms pushed them toward alternative working-capital sources. This is exactly why structure behind non-dilutive capital matters so much.

The Lump-Sum Trap

One of the biggest mistakes I see is taking the full approved amount upfront just because it is available.

I understand the instinct. It gives people a sense of security. But just because your business qualifies for a million dollars doesn't mean you have to take it all.

I compare it to maxing out a credit card. The money is there, so it feels safe. Then the payback starts pulling on your business before that money has generated anything.

The moment they take capital upfront, that's the moment they start paying for the capital. If you are not using that capital in the next 30 to 45 days, you shouldn't be taking that capital up front.

I have seen the damage directly. We helped an apparel brand that had become unprofitable during slower seasons because it was remitting close to 25% of daily sales on a lump-sum loan it had not fully deployed. We restructured the capital into 60-day tranches and stretched it out to a longer payback period, so the remittance would not be as severe. That gave the business room to breathe again.

I have also seen a scaling consumer brand generating over $20 million in revenue take excess capital just in case. It sounded conservative. In practice, the daily remittances kept draining the bank account and trapped the company in a cycle of needing to borrow more.

This is why I am such a big believer in tranching it out and taking it as needed. Line up the capital with real supply chain milestones. Draw the first piece for the deposit. Draw the second piece when the final payment is due. If you need marketing capital, wait until the goods are close enough to arrival that the spend can work right away.

I have seen brands bridge a 90-day production gap this way very effectively. They might take the first draw for roughly 30% of the order, then add another $200,000 or $300,000 later for the balance, with remittance blending up as new tranches are added. That keeps them from remitting toward a balance while the money is still just sitting in the bank account.

At Paperstack, we built our revolving facility around that logic. Brands can draw every 45 to 60 days as needed. We charge a flat fee on deployed capital, not on the unused part of the line. I think that is a much healthier structure for a growing brand.

How I Tell CFOs to Compare APR and Flat Fee

Start with Timing and Your Own Data

Do not start with the rate card. Start with the movement of cash.

When does the supplier deposit leave? When is the final balance due? When do the goods ship? When do they land? When can marketing start? When does Amazon release funds? When does wholesale cash actually hit the account? Once you map that out, the right structure becomes much easier to see.

Then back it with the data. Show the lender 12, 24, or 36 months of history if you have it. Show your seasonal pattern. Show your lowest and highest inventory levels. Show how marketing spend scales. Show how a specific capital injection turns into top-line revenue. Tell the story to the lender and back it with historical performance.

I also do not think finance should make this call in a vacuum. CFOs need to sit with the marketing team and understand the efficiency curve. Know the lowest acceptable ROAS. Know whether the business needs profitability on the first order or whether the payback comes through LTV.

Model the Downside, Not Just the Base Case

This is where my leadership philosophy comes in. Unapologetic optimism isn't about blind positivity - it's about discipline.

One of our brand partners got hit with new import tariffs that tightened landed cost overnight. We did not freeze. We ran conservative, most likely, and optimistic scenarios. We looked at unit economics, supplier relationships, pricing flexibility, and customer retention if prices had to move.

That gave the team options. They kept ordering at scale and maintained supplier relationships while competitors hesitated. When the market stabilized, they were one of the few brands still fully stocked and they captured meaningful market share.

That is how I think CFOs should evaluate APR versus flat fee too. Do not model one clean average month. Model the messy months.

Pressure-Test Stockouts Too

I say this often because I think the market still gets it wrong. Selling out is a financial failure or operational failure unless it was planned as a limited-edition drop.

From the outside, a stockout can look exciting. From the inside, it creates stress fast. I have seen a roughly $5 million wellness brand go viral and sell out on Amazon, only to get hit with weaker search ranking after the stockout. I have also seen an approximately $10 million wellness brand burn through inventory so quickly that it had to pause expansion into new channels just to protect its core DTC customers.

From the outside, it might look like a celebration. From the inside, it's a massive pressure internally operationally for the team. Marketing has to stop campaigns that were working. The CFO may need emergency financing for a restock. The business may end up using expensive air freight and damage its unit economics.

None of that shows up in the headline APR.

I care who is still with you after the funding lands too. You should not have to re-explain your business every time you need support. The best capital partners act more like collaborators than financiers.

My Bottom Line

APR belongs in the model. I would never ignore it.

But for e-commerce and CPG brands, the real decision sits deeper than that. You need to understand the true dollar cost upfront, the remittance mechanics, the use of funds, the covenants, and whether the provider understands the whole business.

The market is moving this way for a reason. Allied Market Research estimates the global revenue-based financing market was about $6.4 billion in 2023 and could reach roughly $178.3 billion by 2033. CFOs are asking for more flexible capital because the old templates do not fit modern commerce.

So if you remember one thing from this article, let it be this: do not ask only, "What is the APR?" Ask what the capital really costs in dollars. Ask when you will use it. Ask how the remittance behaves in a slow month. Ask whether the provider sees the whole business.

That is how you evaluate cash flow quality. That is how you get alignment - not just access. And that is how capital starts working with your business, not against it.

Frequently Asked Questions

How can we accurately forecast cash flow when revenue-based remittances fluctuate daily?

You forecast it as a variable cost tied directly to top-line volume. Since remittance is a fixed percentage of daily receipts, your cash flow coverage ratio remains naturally protected. If sales dip, the cash drain slows proportionally. Model your baseline, but stress-test the maximum monthly caps to ensure liquidity holds.

Does RBF make sense if our primary bottleneck is delayed wholesale payouts?

Yes. Roughly 60% of firms seek alternative capital due to extended terms, and 50% wait over 30 days for receivables. Unlike rigid invoice factoring, RBF underwrites your entire multi-channel revenue. This lets you fund DTC seamlessly while waiting for retail invoices to clear.

Will taking on short-term RBF debt negatively impact our valuation for a Series B?

No. In fact, it protects your cap table. You should always reserve equity for unproven experiments. By using non-dilutive RBF for repeatable inventory turns and proven marketing channels, you maintain higher growth velocity without surrendering shares.

At what gross margin threshold does the implied cost of RBF become a risk to growth?

I tell CFOs to look at unit economics first. If your gross margins sit below 30%, flat-fee RBF might squeeze your operating cash too tightly. But if you hold 50% to 70% margins, the predictable dollar cost of RBF easily absorbs into the inventory cycle, protecting your cash flow during any rapid seasonal scaling.