CFOs ask me this all the time: is revenue-based financing smart capital, or just a more expensive loan with better branding?

My answer is straightforward. It can be a very good tool. It can also create pressure fast. The outcome depends on the structure behind non-dilutive capital, not the headline pitch.

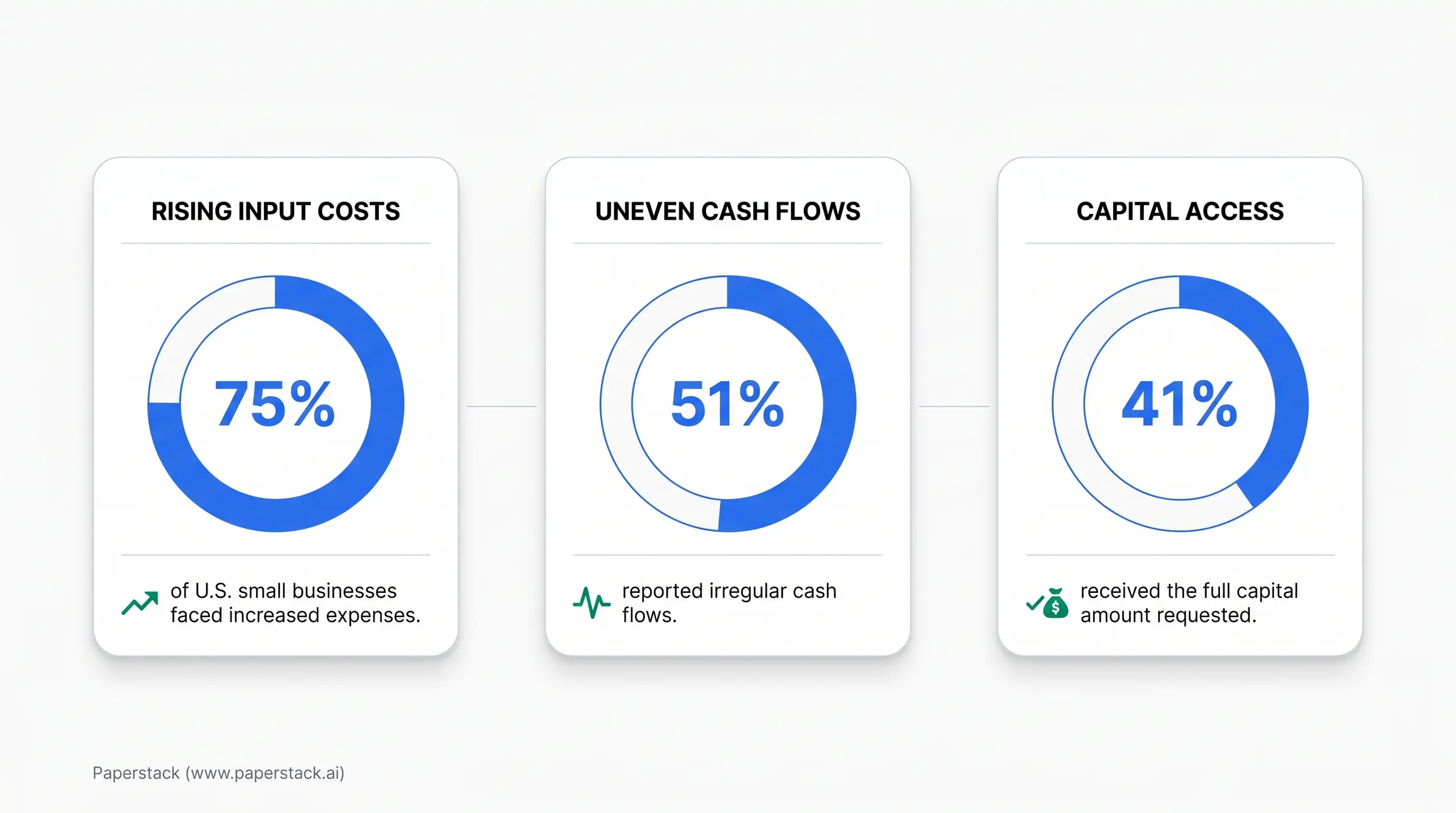

This matters even more right now. Recent Federal Reserve survey data shows 75% of U.S. small businesses faced rising input costs. The same survey found 51% reported uneven cash flows. And when businesses went looking for capital, only 41% received the full amount they requested.

That was one of the clearest examples of the systemic lending gaps in this market. Traditional underwriting was built for factories, equipment, and old-school small business lending. It was not built for CPG brands, Amazon payout delays, or a business where marketing spend is an investment engine.

So if you are a CFO evaluating revenue-based financing, this is how I would look at it.

What Revenue-Based Financing Is Actually Solving

For most e-commerce brands, the problem is not a lack of demand. The problem is timing.

You pay suppliers before inventory lands. You fund marketing before cash comes back. Amazon holds payouts. Wholesale may pay on longer terms. Payroll, rent, shipping, and software do not wait for your cash conversion cycle to catch up. A lot of times, the business is healthy. The timing is not.

That is why I say growth isn't just about how much you sell, it's about when you sell it. Timing drives working capital stress. Timing also decides whether growth feels smooth or chaotic.

Revenue-based financing is meant to bridge that timing gap. In plain English, you get capital upfront and repay it through a share of revenue or bank deposits until a fixed amount is paid back. The appeal is obvious. Repayment can move more in line with performance than a rigid fixed-payment loan.

But that alone does not make it good. If the remittance is too aggressive, if the provider ignores part of your business, or if you draw too much too early, the structure can work against you. That is why I focus so much on cash flow quality. I care about the predictability, timing, and sustainability of how money moves through the business. For e-commerce and CPG, that is the real signal of resilience.

The Pros of Revenue-Based Financing

It Protects Equity for the Things Equity Should Fund

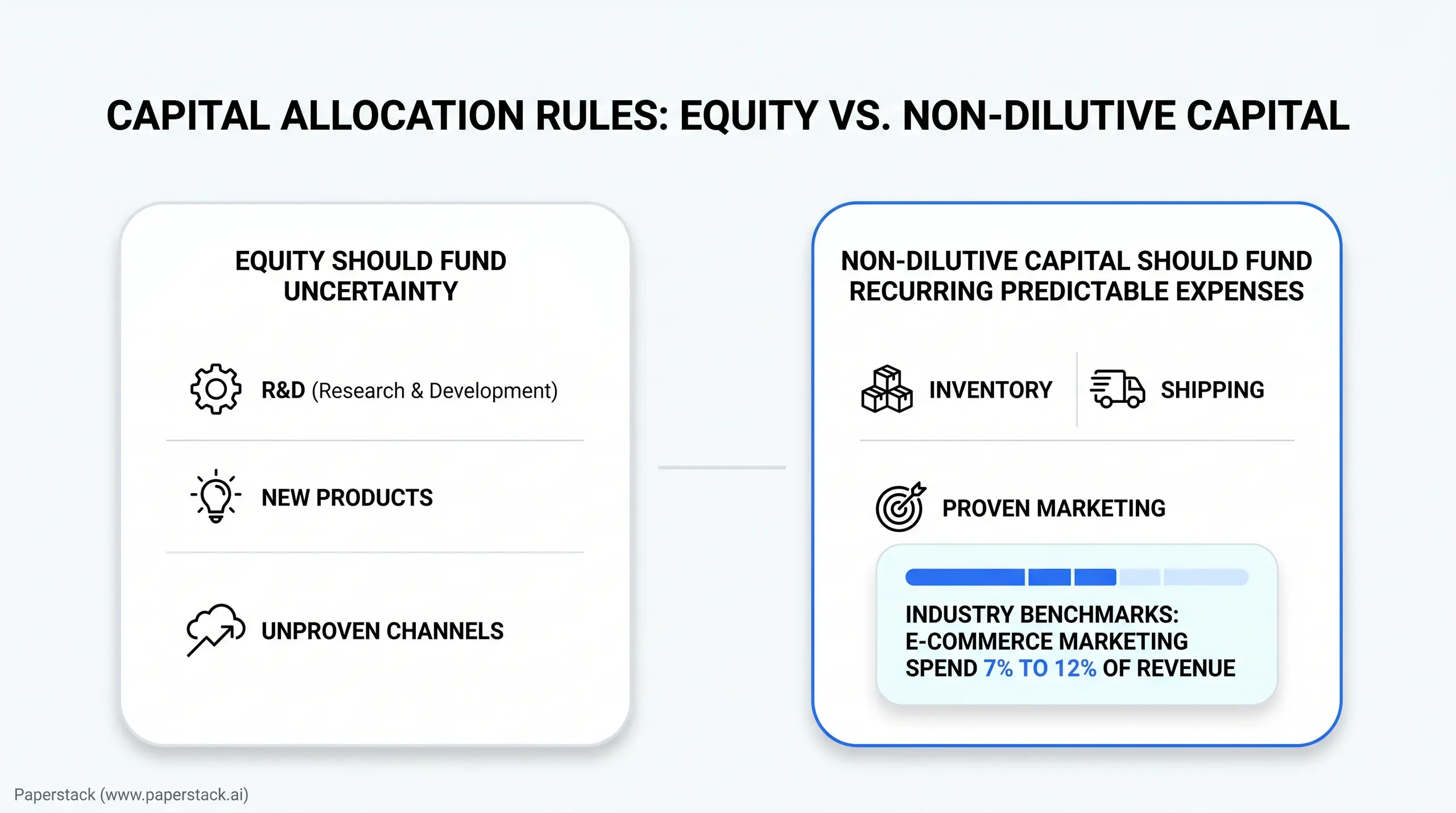

I have a strong view here. The most expensive capital that you can use for inventory or predictable marketing is equity.

Equity should go toward uncertainty. New product development. R&D. New channels where ROI is still unclear. Those are the places where you are buying time, experimentation, and optionality.

Recurring expenses are different. Inventory, shipping, and proven advertising usually sit inside a more measurable system. Industry benchmarks often put e-commerce marketing spend around 7% to 12% of revenue, and high-growth brands can push closer to 20%. In my experience, once a brand is scaling seriously, marketing often becomes one of the top three expense categories alongside inventory and shipping. If you know your ROAS, contribution margin, and payback profile, using non-dilutive capital there can be much more disciplined than giving up ownership.

There is one important exception. If a founder is very early, has no real credit history, and is still testing product-market fit, equity may still be the right tool even for initial inventory. But once the business has a track record, CFOs should be very careful about burning expensive equity on repeatable working capital needs.

It Can Match the Way E-Commerce Cash Actually Moves

This is the biggest operational benefit.

A fixed loan payment may look neat in a model. Then a slower month hits. Amazon pushes a payout. Wholesale cash comes in later than expected. A promotion underperforms. Suddenly the "clean" debt structure becomes the source of stress.

A well-built revenue-based facility can flex better. I saw this clearly with a CPG brand we worked with that had strong repeat customers, healthy margins, and steady month-over-month growth. Their real constraint was cash flow timing. They had to pay suppliers 60 days before inventory arrived, then wait weeks for Amazon to release payouts. Their revenue was spread across Amazon, Shopify, and wholesale.

Other providers looked at one channel at a time. That pushed them toward multiple lenders with different repayment schedules. One provider would consider Shopify. Another would factor wholesale. A third would look at marketplace sales. The result was more pressure, not more clarity.

By underwriting the total performance of the business, they were able to consolidate financing into one source. That mattered. At the same time, they had to decide whether to say yes to strategic retail partnerships or preserve inventory for DTC and pull back on marketing. With the right structure, they did not have to make a false choice. They could support both.

That is what alignment - not just access - looks like in practice.

It Works Better for Asset-Light and Omnichannel Brands Than Traditional Bank Models

This is the part many CFOs already feel, even if they have not said it out loud. The market still favors collateral-heavy businesses.

The approval bias toward secured loans over general unsecured business loans tells you a lot. Asset-light e-commerce brands end up squeezed because the traditional system is still looking for hard assets first. I have seen brands with up to $5 million in revenue get pushed back toward personal lines of credit that are too small for what the business actually needs.

On top of that, traditional loans often come with personal guarantees, slow approval cycles, and inventory-on-hand covenants. That last one drives me crazy. A bank may want to see inventory sitting there as collateral. But for the brand, keeping product in a warehouse can be costly. Seasonality changes. collections move. Storage costs build. The business needs to turn inventory, not admire it.

This is also why I like looking at the whole business, not a narrow slice of it. A B2B channel can make a DTC brand structurally stronger. I have seen brands sell in bulk to banks and law firms for corporate gifting. When the product is personalized with a logo, the brand can often ask for an upfront deposit because that inventory cannot be easily resold. That improves cash flow. It also creates a second benefit: you are often acquiring customers at someone else's cost when recipients later come back and buy directly.

A lender that ignores those channels is missing real stability.

It Gives You More Control Over When Capital Enters the Business

I understand why a large approval feels like a win. It gives peace of mind. It feels like the brand is prepared.

The challenge is simple. If you take too much money upfront, you start carrying the cost of that capital before it is doing anything useful for you. You have to understand what that does to margin and to the bottom line.

I saw this with an apparel brand doing around $10 million in revenue. They had been pre-approved for roughly $1 million in working capital and were remitting more than 17% of daily cash flow to service it. The issue was not the size of the approval. The issue was that they did not need the full amount right away. So from day one, cash was leaving the business while a large part of the capital sat idle.

When we analyzed the operating cycle, the immediate need was closer to $300,000. Then they needed another $500,000 in 60 to 90 days. Structuring the capital around those milestones changed the economics. They did not have to carry the cost of that capital during the waiting period.

That is why I keep saying: just because your business qualifies for a million dollars doesn't mean you have to take it all. I prefer revolving facilities and tranche-based draws. Draw the 30% manufacturing deposit when it is due. Draw the balance when goods leave the warehouse. Pay for deployed capital, not idle comfort. And if a brand has a breakout month, I like monthly caps so we don't penalize them for growth.

It Can Help You Stay Decisive When Volatility Hits

My leadership philosophy is unapologetic optimism. People sometimes hear that and think I mean blind positivity. I do not.

Unapologetic optimism isn't about blind positivity - it's about discipline. It means building options before you need them.

I saw this with a brand partner that got hit by new import tariffs. Landed costs jumped quickly. A lot of finance teams in that spot would freeze inventory orders and cut marketing immediately. We took a different route. We modeled conservative, most likely, and optimistic scenarios. We looked at unit economics, whether supplier costs could be shared, and what customer retention would look like if prices had to move.

That work did not remove uncertainty. It created options. Because the brand had a flexible capital plan behind those options, they kept ordering, maintained supplier relationships, and stayed in stock while competitors hesitated. When conditions stabilized, they captured market share because they were ready.

That is one of the best uses of flexible capital. It helps you make disciplined decisions under pressure instead of defaulting to fear.

The Cons of Revenue-Based Financing

It Can Get Expensive Fast

Let's start with the obvious point. Revenue-based financing is often more expensive than strong bank debt.

That does not mean it is bad. It means you need to be honest about what you are paying for. Speed has value. Flexibility has value. Omnichannel underwriting has value. A structure that grows in rhythm with your brand has value. But the headline rate alone never tells the full story.

Terms are the keys. I want to know the actual total cost of capital. That means fees, admin charges, wire costs, underwriting fees, and anything else buried in the agreement. A low-looking offer can get expensive very quickly once the hidden mechanics show up.

If you qualify for a truly flexible, low-cost bank line that fits your business model and does not box you in with bad covenants, you should absolutely evaluate it. Revenue-based financing earns its place when the structure matches your operating reality better than the alternatives.

A Bad Remittance Structure Can Put Pressure on Liquidity

Two offers can look similar and behave very differently once the business starts moving.

This is where CFOs need to slow down and read the mechanics. Ask about minimum remittances. Ask about maximums. Ask whether there are monthly caps. Ask what happens in your strongest month and what happens in your weakest one. You do not want a structure that drains a full month's payment in the first week of a strong sales period. You also do not want a minimum payment that becomes painful during slower months.

You also need clarity on how revenue is being measured. For wholesale, does the provider count revenue when a draft order is created, or only when cash lands in your account? For Amazon and wholesale-heavy businesses, taking repayment from bank deposits often makes more sense than taking it from online sales snapshots.

And be careful with stacked lenders. Having multiple lenders on your capital stack might look like a risky business to the next financing partner. It also creates blind spots. That matters more in the current market. Federal Reserve survey data shows 41% of denied applicants cited excessive existing debt in 2024. Structure can push you into that category faster than many teams expect.

It Is a Poor Fit for Experimental Spending

Revenue-based financing works best when the path from capital to revenue is clear.

If you are buying repeat inventory for proven SKUs, bridging shipping costs, or scaling a paid channel where you understand your efficiency curve, great. That is exactly where this tool can be useful.

If you are testing a new product, a brand-new channel, or a strategy where attribution is still messy, I would be much more cautious. I want to see the math. Over a 12, 24, or 36-month view, how does this capital injection turn into top-line revenue? If the answer is mostly hope, you are using the wrong tool.

That is why I keep coming back to the same principle. Equity capital is used for R&D purposes. Non-dilutive capital is for recurring expenses. The cleaner that line is, the healthier your capital stack usually becomes.

It Will Not Fix a Broken Operating Rhythm

This is the most overlooked downside.

Revenue-based financing can support a healthy business. It cannot repair a company where marketing, inventory, and cash flow are consistently out of sync. I see this all the time. One team is driving demand. Another is managing production. Finance is watching liquidity. If those calendars are not aligned, the business can still end up in a crunch even when sales look strong.

I am very direct about stockouts. Selling out is a financial failure or operational failure when it happens because capital planning broke. It should not be celebrated when the product is sold out and the customer cannot actually buy. You have already paid to acquire that traffic. Then the shopper lands on the page, sees the item is gone, and leaves. Now you have to rebuild the relationship with the customer and spend again to win them back.

There is more damage under the surface. Fixed costs keep running. Warehouse rent does not pause. Marketing teams lose momentum because they have to shut off campaigns they worked hard to scale. On marketplaces, the hit can be even worse. I saw a wellness brand doing around $5 million in revenue go viral and sell out on Amazon. Their ranking dropped, visibility fell, and regaining that position was hard. I also saw a brand get an unexpected viral moment during the holidays, run out of inventory, and damage trust with customers it had worked hard to attract.

And when external disruptions hit, you still need operating discipline. If there is a port strike or a manufacturing delay, cutting marketing and promotional discounts may be the right move. Preserve margin. Stretch the inventory you have. Sometimes the best growth decision is to slow demand for a few weeks and lean harder into existing customers, email, upsell, and AOV.

Capital helps. It does not replace rhythm.

How I Would Evaluate a Revenue-Based Financing Provider

If I were sitting in your chair, I would start with a simple question: does this provider understand my full business, or are they underwriting a single channel and pretending that is enough? If Shopify is 30% of your revenue and the other 70% comes from Amazon, wholesale, and retail, I want the partner looking at the whole picture.

Then I would dig into the mechanics. I want the actual total cost of capital. I want to know how remittance is calculated, whether there are monthly caps, and how the structure behaves in both a slow month and a big month. I want clarity on how wholesale revenue is treated and whether funds go to my bank account or are paid directly to suppliers or platforms. That changes control.

I also want to know how the relationship works after funding. Will I keep the same contact, or get passed to another department the moment the deal closes? That matters more than people think. In volatile periods, you do not want to re-explain your business every time you need support. The best partners act more like collaborators. They help you forecast, scenario-plan, and structure the growth capital in a way that it empowers the brand.

Finally, bring your own math. Know your minimum acceptable ROAS. Know whether your business needs first-order profitability or whether LTV supports a longer payback. Know your deposit patterns. Use your own historical data when negotiating remittance caps. A good provider should welcome that conversation.

My Rule of Thumb

I like revenue-based financing when the use of capital is predictable, the cash conversion logic is clear, and the structure is built around the operating rhythm of the business. It can be a very strong fit for inventory, shipping, and proven marketing spend. It can also be useful when you want one partner to underwrite the full performance of an omnichannel brand instead of carving the business into pieces.

I prefer equity for true experimentation. New products. R&D. Unproven channels. That is where uncertainty belongs. And if you can secure bank debt that is low-cost, fast enough, and flexible enough for how your business actually works, that should stay on the table.

I think about commerce finance like structural engineering. Good capital should support the business quietly. It should fit the timing of your cash flow. It should help you make better decisions. And it should leave you with room to operate when the market gets noisy.

That is the real test. When capital starts working with your business, not against it, you feel it in planning, in inventory, in marketing, and in the confidence of the whole team.

Frequently Asked Questions

How does revenue-based financing affect our balance sheet under GAAP?

Under GAAP, revenue-based financing is typically treated as a liability, not equity. Because repayments fluctuate with daily sales, exact amortization forecasting is complex. You must record the initial principal and accrue the estimated interest expense over the projected repayment period, continually updating your liquidity models to ensure accurate financial reporting.

Can revenue-based facilities be subordinated to existing traditional bank debt?

Yes, but it requires careful negotiation. Federal Reserve data notes 41% of denied applicants cited excessive debt. While banks demand a primary UCC-1 lien, a strong revenue-based partner often accepts a subordinated position via an intercreditor agreement, provided your overall working capital utilization remains healthy.

How should we calculate the true cost of capital for a revenue-based offer?

Forget the headline flat fee. You must calculate the implied APR. If you pay a 6% fee but remit the balance in three months due to fast inventory turnover, the annualized cost is staggering. CFOs must run sensitivity analyses on repayment speed to uncover the true cost of capital.

Does utilizing revenue-based capital impact our company valuation during an M&A exit?

It actually protects valuation. By avoiding early equity dilution for inventory, you preserve the cap table. When buyers evaluate the business, they will treat the remaining revenue-based balance as standard working capital debt, deducting it from the enterprise value. Just ensure no punitive prepayment penalties exist in your agreements.

How do we negotiate remittance caps to protect liquidity during Q4 revenue spikes?

High-growth brands can be punished by their own success. If Black Friday spikes your revenue, an uncapped daily remittance will severely drain liquidity. I always advise CFOs to negotiate absolute monthly dollar caps. This ensures that once your principal repayment hits a certain threshold, the excess cash stays in your business.