Most people saw a celebrity partnership. I saw a finance stress test.

I spend my life in the mechanics of growth. Cash timing. Inventory cycles. Capital structure. The unsexy stuff that decides whether momentum compounds or stalls.

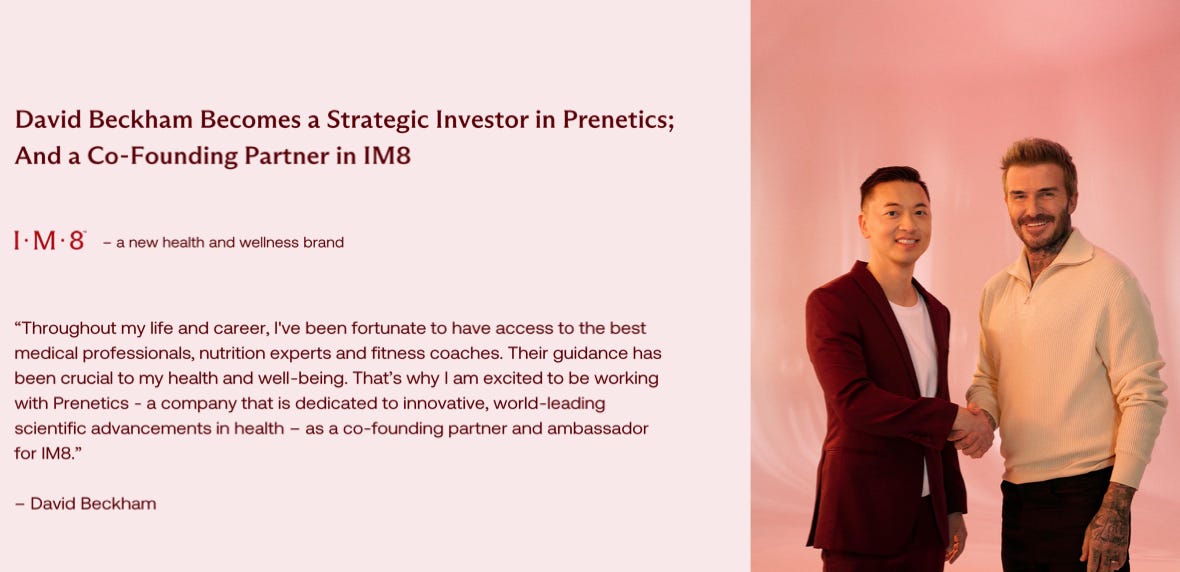

So when Prenetics partnered with David Beckham to co-found IM8, I paid attention. Not because of the celebrity. Because of what the numbers did right after.

The revenue curve: from $30M reality to $200M guidance

Prenetics was already growing before IM8 launched.

They reported $21.7M in 2023 revenue. They also disclosed a 65.2% year-over-year increase versus 2022.

In 2024, the company reported $30.6M in 2024 revenue. They reported that as 40.9% growth over 2023.

Those years also came with losses. Prenetics disclosed an adjusted net loss of $28.4M in 2023. That's a useful reminder for any CFO reading this: growth stories often start before the model is perfect.

IM8 launched in November 2024. By Q3 2025, Prenetics reported $23.6M in Q3 2025. They also reported a 568% year-over-year jump.

IM8 was on track to reach $120M in ARR within 12 months of launch. Prenetics projected $180M - $200M FY2026 guidance driven by IM8.

That's the headline transformation. A company doing about $30M a year guiding to almost $200M. In one year.

What does that kind of ramp do to your cash plan?

Beckham's real contribution was trust that converts

Here's what I find interesting from a finance perspective.

When Beckham joined, Prenetics had a market cap under $100M. Someone with his profile could have taken them private. Instead, he joined as a strategic investor and stayed in the public markets.

Since announcing the partnership, the stock went from around $6 to a peak near $23. Market cap rose to around $260M. His exact investment amount was never disclosed.

At Beckham scale, the biggest asset isn't just money. It's trust.

In consumer, trust is a growth lever you can actually feel. It tends to lift conversion rates, ease CAC pressure, and increase repeat behavior. It also opens doors with retailers, suppliers, and talent.

You can't book "trust" on the balance sheet. But you see it in cash flow when demand starts compounding.

If trust spikes, can you stay in stock long enough to monetize it?

Hypergrowth squeezes timing before it rewards strategy

I treat finance like structural engineering.

When the beams are aligned, growth feels smooth. When they're off, speed exposes every crack.

Step-function growth puts pressure on timing. Revenue can jump overnight. Your supply chain can't.

Inventory turns growth into a prepayment problem

Product businesses fund growth upfront.

You pay suppliers before the product is ready. You wait through production. You wait through freight. Then you sell. Then you get paid.

When demand accelerates, that gap becomes the constraint. You can be "winning" on the top line and still be cash tight.

We worked with a CPG brand that had strong repeat customers and healthy margins. They sold out every launch, but their constraint was cash flow timing. They had to pay suppliers 60 days before inventory arrived, and they waited weeks for Amazon payouts to hit.

Traditional lenders often read that pattern as volatility. I read it as momentum trapped in a cycle.

Multichannel revenue can hide the real cash picture

Most brands at $5M - $50M revenue aren't single-channel anymore. They sell on Shopify, Amazon, and wholesale, all with different payout timing.

This is where capital decisions can quietly create chaos.

Some providers only underwrite Shopify revenue. Others only underwrite Amazon. Then you add factoring for wholesale. Now you're juggling three repayment schedules, three dashboards, and three sets of rules.

We've seen teams get stuck in that "patchwork stack." It adds pressure and steals attention. Consolidating into one clear source of capital is often the difference between stable growth and constant firefighting.

Selling out is expensive, even when it looks like a win

I'm direct about this: it shouldn't be celebrated when the product is sold out.

When a loyal customer lands on your product page and sees "out of stock," you just paid CAC to disappoint them. Then you pay again to rebuild the relationship with the customer.

I've seen a brand go viral during the holidays and run out of stock. From the outside it looked like a win. Inside, it created broken trust and higher acquisition costs later.

If IM8's demand curve looked anything like the public numbers suggest, staying in stock had to be part of the financial plan. You don't guide to $200M by burning consumer trust.

Why banks still miss modern commerce

This is the part that's personal for me.

In banking, I kept seeing strong consumer brands get declined. Not because they were weak businesses. Because underwriting was built for asset-heavy industries.

One example was a DTC beverage brand doing over $3M in annual revenue. Customers loved them. Margins were healthy. Cash flow was steady.

They still got declined because they had no hard assets, revenue was seasonal, and marketing spend looked like an "expense." In e-commerce, marketing is often the investment engine. In many bank models, it reads like instability.

That's the systemic lending gap. It shows up right when you need speed.

For you as a CFO, the takeaway is practical. Choose capital partners who understand your cash flow cycle and your channel mix. Don't waste time trying to fit an asset-light business into a factory-era template.

How I think about underwriting: cash flow quality and operating rhythm

At Paperstack, we underwrite the whole business across channels. We care about cash flow quality.

Cash flow quality is the predictability, timing, and sustainability of how money moves through your business. It's the closest thing e-commerce has to "collateral."

This lens also changes how you treat marketing.

Many growing brands invest 15% to 25% of annual revenue into marketing. It's usually a top-three expense right next to inventory and shipping. The question isn't "Do you spend?" The question is "Does that spend pay back, and how fast?"

That's why we look at ROAS, payback timing, and contribution margin. Marketing can fund growth. It can also create a cash crunch if it's out of sync with inventory and payouts.

Paperstack started as a CFO analytics platform for real-time visibility. Then founders gave us the same feedback again and again: visibility is great, but they needed capital to act. That's when we pivoted to revenue-based financing. Data alone doesn't move a business forward - capital does, when it's deployed with insight.

Capital structure: keep flexibility when the slope changes

Fast growth tempts teams into rigid decisions.

You take a full lump sum because it feels "safe." You accept terms that look cheap but pull cash too aggressively. You stack lenders by channel and create repayment chaos.

Structure matters more than the headline rate.

Equity and non-dilutive capital have different jobs

I reserve equity for R&D and new product launches. Those are bets.

Recurring expenses like inventory and payroll need a different tool. Funding them with equity can create dilution that you feel for years.

There's an exception I always mention. Early-stage influencers with no credit history may need initial equity to test inventory before there's any track record. Once revenue is predictable, the stack should evolve.

Draw capital in tranches, the same way you manage inventory

I compare taking a full lump-sum loan to maxing out a credit card personally. You create pressure you didn't need. You might also pay for capital that sits unused.

Just because your business qualifies for a million dollars doesn't mean you have to take it all.

Paperstack's Capital Wallet is built around this idea. We provide growth capital and offer a revolving commitment, often $1M - $3M, and brands draw in tranches as needed.

A common cadence is $100K - $500K drawn every 45 - 60 days. That structure lets you match draws to supply chain milestones. If your manufacturer needs a 30% deposit, draw the deposit. Wait to draw the balance until goods ship, so you're not paying for capital during the production lead time.

We price on deployed capital, not unused commitments. We also don't charge origination fees or hidden admin fees. CFOs deserve clean math.

Terms are the keys. Structure decides whether capital supports your rhythm or interrupts it.

Remittance needs guardrails

Revenue-based repayment can protect cash flow, but only if the mechanics are built well.

Monthly repayment caps matter. They prevent the "penalty of success," where a huge revenue month triggers an aggressive paydown that drains working capital.

You should also understand where repayment is sourced. For wholesale and Amazon businesses with long payout cycles, tying remittance to daily bank deposits can create better alignment than tying it to online sales.

Due diligence: the questions that actually protect you

If you're evaluating non-dilutive capital, don't stop at the headline offer. The structure behind non-dilutive capital is where the real risk lives.

Start with total cost. Ask for every fee in writing, including anything charged on unused capital. A low headline rate can get expensive fast once origination, admin, or processing fees appear.

Then confirm what revenue they underwrite. If they only count one channel, they're missing your reality. That often forces you into multiple lenders, which makes cash flow harder to manage.

Get precise on remittance thresholds. Minimum payments can hurt in slow months. Overly aggressive maximums can drain cash in strong months. Predictability matters more than marketing language.

If you have wholesale, clarify how they treat timing. Some partners count wholesale revenue when an order is created. Others only count it when cash hits your bank. That difference changes your forecast.

Ask how funds are deployed too. Money landing in your bank account gives you control. Money paid directly to suppliers can limit flexibility when plans change.

Finally, ask what support looks like after you sign. Will you keep relationship continuity, or get handed off? Financing should feel like a long-term operating partnership.

Alignment matters more than speed. Do the terms still work in your slow months?

If your brand hits an "IM8 moment," protect the system

You don't need a celebrity partnership to trigger step-change growth. A retail win, a marketplace breakout, or a viral moment can do it.

When it happens, start with cash and timing.

Forecast weekly, not monthly. Separate revenue from cash receipts. Map supplier payments, production lead times, and payout timing by channel. Your P&L can look healthy while your bank balance tells a different story.

Then force alignment between marketing, inventory, and finance. When those calendars aren't in sync, cash gets trapped and margins get squeezed. Inventory sits too long or sells too fast. The business gets pushed into discounting and emergency funding.

Get clear on your growth engine, too. Some models rely on first-order profitability. Others rely on lifetime value. That decision dictates what "smart" marketing spend looks like, and when you should pull back and focus on AOV instead of acquisition.

And if inventory is delayed, slow demand on purpose. Lower marketing spend. Remove promotional discounts. Protect your in-stock position. Selling out creates a longer recovery because you have to win the customer back.

Closing: trust lights the match, finance keeps the fire controlled

Prenetics reported $30.6M in 2024 revenue. IM8 helped drive a projection of $180M - $200M in FY2026. That's a massive re-rating in a short window.

Trust can ignite demand. I believe Beckham's trust did exactly that.

Your job as a CFO is to build the architecture that can hold the growth. The capital stack. The repayment mechanics. The forecast cadence. The operating rhythm.

That's the future we're building at Paperstack, with a mission to democratize access to working capital for a million merchants. Today, about 84% of our customers are businesses run by women and diverse founders. The goal is simple: capital that grows in rhythm with your brand, so it starts working with your business, not against it.

Because when the slope changes, excitement fades fast. Execution is what stays.

Frequently Asked Questions

How does step-function growth, like IM8's, impact working capital requirements?

Rapid scaling creates a 'prepayment problem.' Even with Prenetics projecting $180M - $200M revenue for FY2026, the cash drag from production lead times can strangle liquidity. You need capital that scales with the order, not just the bank balance, or you risk being 'winning' on the top line while cash-tight.

Should a CFO prioritize inventory availability over short-term profitability during a launch?

Yes. Selling out isn't a win. It's a broken promise that wastes CAC. Prenetics accepted an adjusted net loss of $28.4M in 2023 to build momentum. If supply chain lags, discipline means slowing marketing spend to protect the customer relationship rather than selling empty shelves.

Why is revenue-based financing often safer than traditional debt for seasonal e-commerce brands?

Traditional fixed debt ignores your 'operating rhythm.' Revenue-based options align repayment with cash flow quality - meaning if you have a slow month, you pay less. This prevents the liquidity crunch that rigid bank loans cause when revenue fluctuates but debt service remains static.

How do I model the financial impact of 'intangible' assets like a celebrity partnership?

Don't just model volume. Model efficiency. A trust-based lever - like the one driving 336.5% growth in Q1 2025 - should materialize as lower CAC and higher conversion rates. You can't book trust on the balance sheet, but you must forecast the resulting margin expansion.

What specific 'guardrails' should I demand in a non-dilutive financing agreement?

Demand monthly repayment caps to prevent a 'penalty of success' where viral sales drain working capital. Also, structure draws in tranches (e.g., every 45-60 days) to match supply chain milestones. This ensures you aren't paying interest on capital that sits idle in your account.