In 2026, most growing CPG brands do not have a demand problem. They have a capital problem.

You can have repeat customers. You can have healthy contribution margins. You can have ads that work. And you can still sit across from a bank and hear that your business looks risky.

I saw that pattern for years when I worked in banking. It is a big reason I built Paperstack.

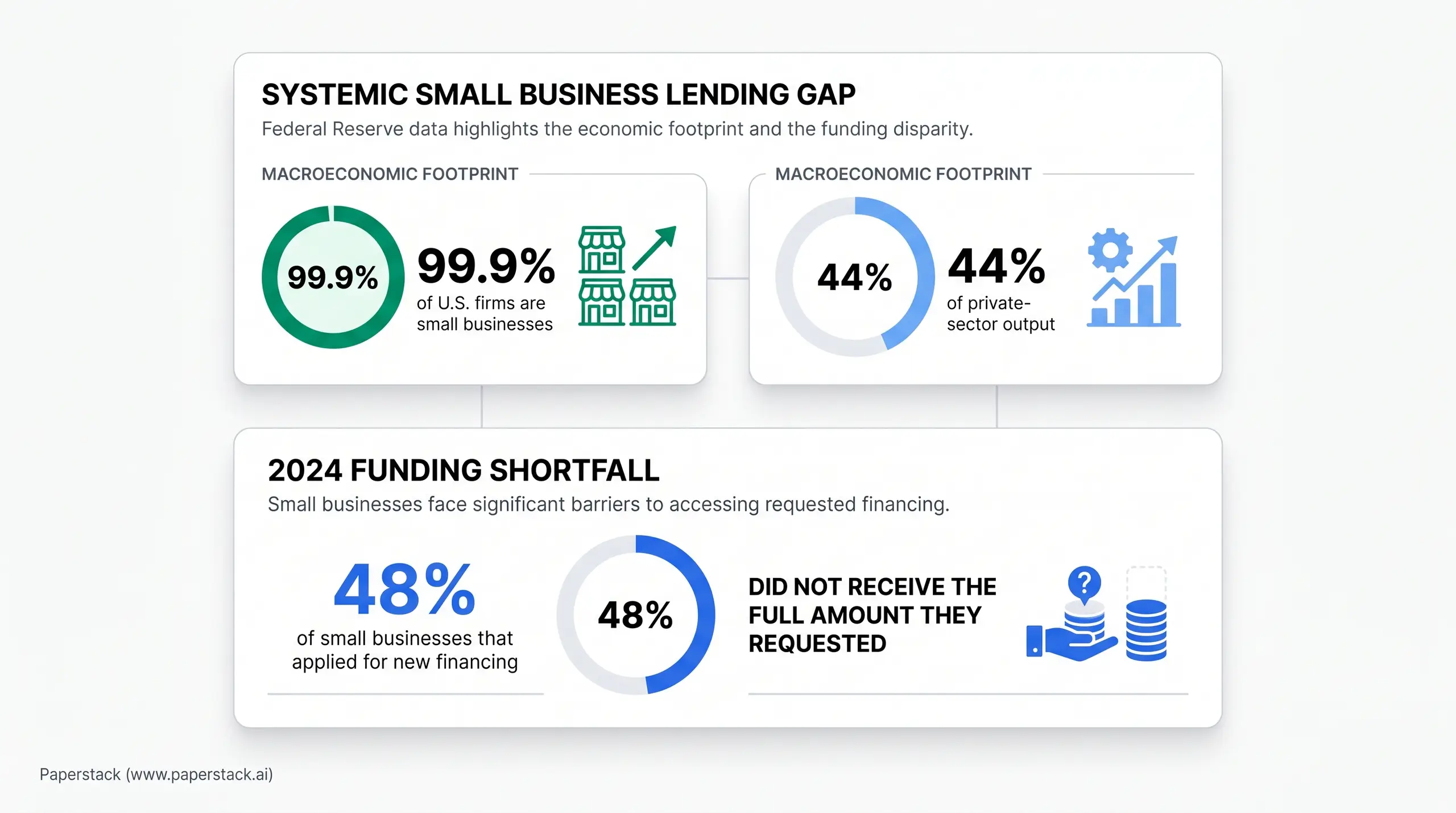

This is a much bigger issue than people think. Federal Reserve data shows small businesses make up 99.9% of U.S. firms and generate roughly 44% of private-sector output. Even so, fewer than 50% of small businesses say their financing needs are fully met. In 2024, 48% of small businesses that applied for new financing did not receive the full amount they requested.

For asset-light CPG brands, the gap gets even sharper. You may be doing millions in revenue, but because you outsource manufacturing and keep the balance sheet light, traditional lenders often read that as weakness. I read it differently. I look at cash flow quality. I want to know how predictable it is, how the timing works, and whether it is sustainable.

Why Banks Still Say No to Healthy CPG Brands

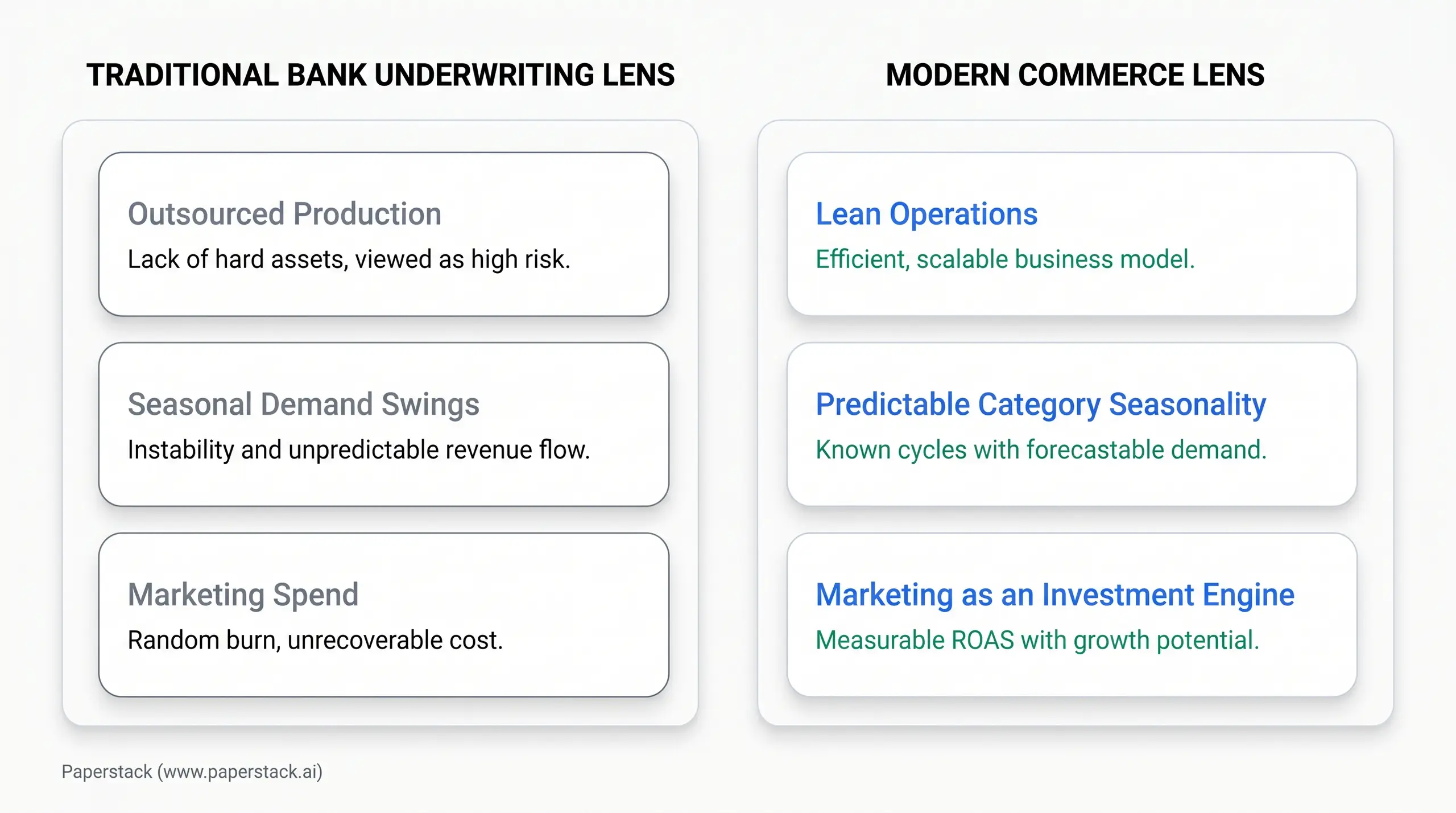

The core problem is simple. The underwriting model was not specifically built for CPG brands..

That disconnect is the systemic lending gap.

Hard Assets Still Drive the Decision

Banks feel comfortable when they can point to equipment, real estate, or some clear form of collateral. Many modern consumer brands do not look like that. They use co-packers. They use 3PLs. They stay lean on purpose.

That operating model makes sense. It helps brands move faster and stay flexible. It just does not fit older credit models very well.

I have also seen brands around the $5 million revenue mark struggle to get a meaningful commercial loan. They may get pushed toward a personal line of credit instead. That is usually too small for the real working capital need. It does not solve the gap between paying suppliers now and getting paid by Amazon, Shopify, or wholesale accounts later.

Marketing Spend Is Still Misunderstood

This is one of the biggest issues for asset-light brands.

A lot of growing CPG companies spend 15% to 25% of annual revenue on marketing. That is not random burn. It is often one of the top expense categories in the business. If a lender cannot interpret that line item properly, the whole conversation goes off track.

I believe marketing spend has to be evaluated as an investment engine. That does not mean every dollar of ad spend is good. You still need the math. You need to know your contribution margin, your CAC, your LTV, your return on ad spend, and the point where efficiency starts to drop as budget scales.

ROAS matters. It tells part of the story. I do not make capital decisions based only on ROAS, and I do not think anyone should. But when marketing is disciplined and repeatable, it should absolutely count in underwriting.

If you want a lender to understand that, bring the history. Show 12, 24, or 36 months. Show that marketing is not just an experiment. Show how a certain amount of capital turns into top-line revenue after all costs. Back it with the data. Show it with the numbers.

Seasonality and Inventory Turnover Get Punished

Banks also tend to look at seasonality and get nervous. Founders look at the same pattern and say, "Yes, that is how this category works."

A seasonal gifting brand should not be structured like a subscription brand. A beverage company with summer-heavy demand should not be judged like a business that has flat revenue every month. Terms are the keys. Covenants need to fit the business model.

I also have a problem with rigid inventory covenants. Some lenders want inventory on hand because it makes them feel protected. For the brand, that can create the opposite outcome. Inventory sitting too long ties up cash. It raises storage costs. It can become dead weight when seasons shift.

Consumer brands need inventory to move. Fast.

This caution from banks has been around for years. Kansas City Fed survey data showed banks tightening standards for small-business loans even while credit quality was largely unchanged. That mindset never fully left.

The Process Itself Can Cost You the Season

Even when a bank is open to the conversation, the structure can still be painful. Personal guarantees. Long approval timelines. In-person meetings. Months of back and forth.

For a founder who needs to place a supplier order this week, that is not a small inconvenience. It can cost the season. It can cost the retail window. It can cost the opportunity to restock before your best-selling SKU goes dark.

What Revenue-Based Financing Should Do Instead

Revenue-based financing should start from how money actually moves through the business.

That is why I focus on cash flow quality. I want to understand predictability, timing, and sustainability. If your customers repeat, your margins hold, and the timing of cash can be modeled, that tells me much more than a warehouse full of inventory.

I think of finance as structural engineering. The job is to build a capital structure that can carry growth without cracking your margins.

Build Around a Facility, Not a One-Time Advance

In my view, the best revenue-based financing in 2026 looks more like a capital wallet than a one-time loan.

When we first started Paperstack, we were building a CFO analytics platform. Founders kept telling us the same thing. They said, "This is helpful, but I need capital to act on the data." That was the moment things became clear for me. Data alone doesn't move a business forward - capital does, when it's deployed with insight.

So when I think about a modern facility, I do not think about one big lump sum dropped into your bank account on day one. I think about a committed line that you can draw in tranches as the business needs it. For more mature brands, that may mean a larger commitment, then smaller draws every 45 to 60 days tied to real uses like supplier deposits, production runs, or marketing pushes that already have a clear return path.

That rhythm matters. If you only need the 30% manufacturing deposit today, draw that amount. Wait to draw the balance until goods actually leave the warehouse. If you will not be using the capital for the next 30 or 45 days, you should not be taking it.

A good facility should also avoid charging you on unused capital. If the money is sitting undrawn, you should not be paying for imaginary flexibility.

Underwrite the Whole Business

One of the biggest mistakes I see is underwriting a specific channel and not the whole business together.

I recently worked with a CPG brand that sold across Amazon, Shopify, and wholesale. Their issue was not demand. Their issue was timing. They had to pay suppliers well before inventory landed, and then they had to wait for platform payouts. Other capital providers wanted to underwrite only one channel or factor only wholesale.

That would have left the business managing three or four lenders at once. Each lender would have its own repayment timing. Each would have its own risk view. Each would want to look only at one slice of the company.

From the outside, that might look manageable. Inside the business, it creates confusion and extra stress on cash flow. If one channel slows, that specific lender may panic and put pressure on the whole company. I have seen how that can create a domino effect.

A capital partner should look at the full business. DTC, Amazon, wholesale, retail. If Shopify is only 30% of your revenue, a lender that underwrites only Shopify is missing most of the picture.

Protect Liquidity When Growth Speeds Up

A good revenue-based structure should protect the brand when revenue jumps.

This is where remittance design matters. I believe in repayment caps. If a brand has a breakout month, I do not want the repayment to suddenly speed up so much that it drains operating cash. We do not penalize them for growth.

That may sound like a small detail. It is not. Fast growth can create just as much stress as a slow month when the structure is wrong.

Repayment source matters too. For brands with wholesale or Amazon-heavy cash cycles, I often prefer repayment tied to daily bank deposits rather than raw online sales. That lines up better with how cash actually lands in the business.

Where Founders Quietly Destroy Margin

A lot of brands do not lose margin because demand disappears. They lose margin because the capital structure forces bad decisions.

Taking Too Much Money Too Early

One of the most common mistakes I see is taking the full approved amount just for comfort.

I understand the instinct. A bigger cash balance feels safe. But if that money is sitting idle, you are still carrying the cost of that capital. It is a bit like maxing out a credit card just because you can. The pressure shows up in daily remittances, in service fees, and in the distraction of servicing capital that is not helping you still.

I have seen a roughly $5 million brand take a $1 million loan and remit more than 20% of daily sales while part of that money was not even being used. Sit down with your accountant. Sit down with your CFO. Map the next bills that are actually due. If the money is going to sit there for 60 or 90 days while product is still in production, you are paying for dead time.

I have also helped an apparel brand that became unprofitable in slow seasons because it was remitting close to 25% of daily sales on a lump-sum facility. We restructured that into 60-day tranches and refinanced the remaining balance over a longer period. The goal was straightforward. Stop costing the business to service capital that was just sitting in the bank account.

Selling Out Is Expensive

I feel strongly about this one. Selling out is often treated like a win. In reality, it can be very expensive.

I worked with a nearly $10 million omnichannel brand that ramped advertising efficiently and sold inventory much faster than expected. The team had to cut ad spend even though the campaigns were working. Then Amazon started going out of stock, and the finance team had to scramble to figure out faster shipping and urgent restocks.

I have seen a similar problem with a wellness brand around the $5 million mark that went viral and sold out on Amazon. The stockout hurt its search ranking and made it much harder to regain visibility.

From the outside, a stockout can look exciting. Inside the business, it creates pressure everywhere. CAC rises because you have to rebuild the relationship with the customer and win them back when inventory returns. Fixed costs like warehouse rent keep running. Marketing teams lose momentum. And if you panic and use air freight or smaller emergency production runs, your unit economics can break fast.

Growth isn't just about how much you sell, it's about when you sell it.

That is why I push teams to align the marketing calendar, the production schedule, and the cash flow cycle. The same timing logic shows up around holidays too. I often tell brands to start their promotions before Black Friday because CAC spikes during the rush, and waiting for the crowd can ruin otherwise good economics.

When a Bank Loan Still Makes Sense

I am not anti-bank. I am anti-misalignment.

If you have hard collateral, a simpler operating model, and enough time to go through a slower process, a bank loan can still be a good tool. The cost may look attractive. The structure may work just fine. Some businesses fit that model well.

Most asset-light CPG brands I talk to do not fit it cleanly. They outsource production. They deal with seasonality. They need flexible access to capital several times a year. They cannot afford a structure that punishes inventory turnover or treats marketing as a warning sign.

For those brands, revenue-based financing usually fits better. But only if the structure behind non-dilutive capital is sound.

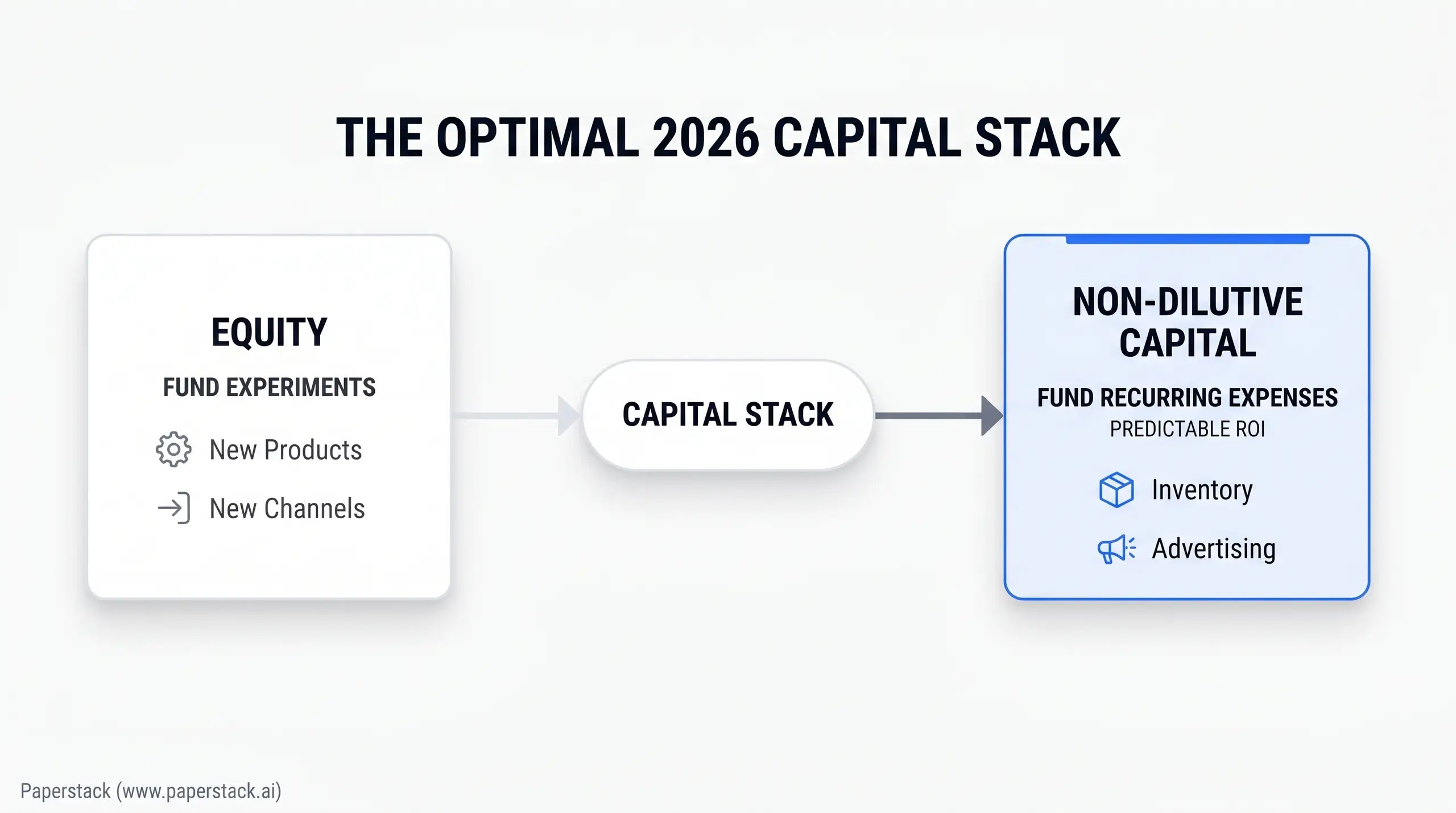

The Capital Stack I Would Build in 2026

A durable capital stack gives each type of capital a clear job.

Use Equity and Non-Dilutive Capital for Different Jobs

I am very clear on this. Equity should fund experiments. Use it for new products, new channels, specific hires, or expansion where the return path is still uncertain.

Use non-dilutive capital for recurring expenses with predictable ROI. Inventory fits that. Advertising often fits that too, if the numbers are there. The most expensive capital you can use for predictable inventory or marketing is equity.

Very early businesses can be different. If you have no credit history and you are still proving market fit, equity may be the right tool for that first stage. Once the business has real operating history, I believe those jobs should be separated much more clearly.

Plan for Volatility Before It Hits

My idea of unapologetic optimism is very practical. Unapologetic optimism isn't about blind positivity - it's about discipline.

I saw this clearly when one of our brand partners got hit by new import tariffs. Landed costs changed fast. A lot of teams in that position would cut marketing and freeze inventory. We took a different route. We ran conservative, most likely, and optimistic scenarios. We looked at unit economics, supplier options, pricing flexibility, and what customer retention might look like if prices moved.

That work gave the team options. They kept ordering while others hesitated. When conditions stabilized, they were in stock and able to capture market share.

The same discipline matters during supply chain disruptions. If there is a port strike or a manufacturing delay, I often advise brands to reduce marketing spend and pull back heavy discounts. Stretch the inventory you have. Protect margin. Use the saved cash for the unexpected out-of-pocket costs that always show up in those moments.

Add Stability Where You Can

If you want better financing options, make the business structurally stronger.

I like seeing DTC brands add B2B or wholesale in a deliberate way. It can reduce seasonality and improve cash flow stability. I have seen brands sell in bulk to banks and law firms for corporate gifting. That can work like funded customer acquisition because the corporate buyer pays for the order, and some of the recipients later become direct customers.

There are practical ways to make that channel stronger too. If you offer personalization, like adding a company logo, it becomes easier to ask for an upfront deposit because the client understands that customized inventory cannot easily be resold.

If you are testing B2B, start small. Reach out to a focused group of local companies and see who responds. Once one office buys, use that relationship to open conversations with other branches. Deliberately diversify revenue to minimize seasonality. That makes the business healthier and easier to finance.

What to Ask Before Signing Any Offer

Do not stop at the headline rate. Go deeper.

Start with the real total cost of capital. Ask about origination fees, admin charges, wire fees, and any fee for changing accounts or adjusting the structure later. A cheap headline can hide an expensive reality.

Then ask how the payments actually work. Is there a minimum that could hurt you in slow months? Is there a cap that protects you in strong months? Use your own history when you negotiate this. Show the lender your high months and low months. Tell the story to the lender and back it with historical performance.

You also need to ask whether the provider is looking at all of your channels or just one. If they only see Shopify and your business also sells on Amazon and through wholesale, they are missing a big part of the picture. Ask how they treat wholesale revenue too. Revenue should count when cash lands, not just when an order draft exists in a system.

Control matters as well. Ask where the funds go. Some providers send money to your business. Others pay suppliers or ad platforms directly. That changes how much control you have over working capital day to day.

And if you already have another lender, project how each provider will affect the cash flow of the business. One aggressive remittance schedule can put stress on the others.

The relationship matters too. Ask who will support you after funding. I care a lot about continuity here. The relationship should not disappear once the deal closes.

My Final View

In 2026, the best capital partner is the one that understands your business rhythm.

If your brand is asset-light, omni-channel, and growing fast, you need more than access to money. You need alignment. You need capital that fits your cash cycle, your inventory timing, and your marketing engine.

That is the real difference between revenue-based financing and bank loans. Bank loans still tend to ask modern brands to squeeze into an older template. Good revenue-based financing starts with the actual operating shape of the business and builds from there.

That is also why I believe the future looks more like a financial operating system than a one-time loan. A durable capital foundation. A structure that grows in rhythm with your brand. A partner that helps you act with more confidence when the next inventory order, tariff shock, or growth spike hits.

That is the kind of capital I believe modern commerce deserves.

Frequently Asked Questions

Why is securing a traditional commercial loan becoming harder for high-growth CPGs?

Banks are structurally retreating from small businesses. Even with stable credit quality, new term loans dropped 8.6% in recent Federal Reserve surveys due to tightening standards. Traditional lenders penalize asset-light models, forcing founders to seek revenue-based financing that actually values cash flow over physical collateral.

How does a revenue-based financing model impact our next venture capital valuation?

It protects your equity by acting as a non-dilutive bridge. By funding predictable customer acquisition and inventory runs with revenue-based capital, you scale top-line revenue without giving up board seats. When you eventually raise a Series A, you negotiate from a stronger position with a much higher valuation.

Can we stack revenue-based financing alongside our existing invoice factoring facility?

Yes, but alignment is critical. Factoring solves wholesale receivables, while revenue-based capital fuels your DTC customer acquisition and initial inventory deposits. A durable capital stack maps specific funding to specific cash cycles. Just ensure your provider understands your subordinated debt structure so daily remittances do not crush operating liquidity.

How does revenue-based financing handle the cash gap when moving to stricter upfront supplier terms?

Tightening supplier terms require a precise capital budget. Instead of draining operating cash, you draw a targeted tranche to cover upfront co-packer deposits. This bridges the critical gap between production and your eventual Shopify or Amazon payouts, keeping your growth engine funded without breaking your unit economics.

Why do profitable, high-velocity brands still face rejection from tier-one commercial banks?

Banks underwrite assets, not velocity. In fact, 48% of small businesses applying for financing in 2024 did not receive their requested amount. Banks view robust marketing spend and seasonal turnover as volatility. Revenue-based underwriting treats these as predictable growth engines, perfectly aligning with asset-light scaling.