I view finance as structural engineering.

Every layer of capital should carry a specific load. In ecommerce, that matters because cash never moves in a straight line. You pay suppliers before goods arrive. You spend on marketing before repeat revenue shows up. Amazon and wholesale may pay you weeks later. If your capital stack ignores that rhythm, your P&L can look healthy while your bank account feels tight.

So when I talk about junior debt, I am talking about discipline. I am talking about structure. I am talking about using another layer of capital only when it has a clear job and a clear payoff.

Why Ecommerce Brands End Up Needing Junior Debt

Junior debt usually sits behind your senior lender in the stack. Because it takes more risk, it usually costs more. So it needs to earn its place. If you cannot explain its job in one sentence, pause right there.

Ecommerce brands reach for this layer because the business is full of timing gaps. Inventory deposits go out now. Revenue lands later. A seasonal brand may make a huge share of annual revenue in one quarter and still need to fund raw materials in the slower months. A multichannel brand may be healthy overall, still every channel pays on a different schedule.

The broader credit market still shows that strain. The Federal Reserve notes that 99.9% of U.S. firms are small, still access to credit is still uneven. In 2024, only 52% of applications were fully approved. Large banks have been especially tight. A Fed analysis found they approved just 58% of small-business loan applications.

I still see brands around $5 million in revenue getting pushed toward personal lines of credit that are far too small for the real need. I also see founders lose time to slow bank processes, personal guarantees, and old-school collateral rules. That hurts when your supplier needs an answer this week, not three months from now.

So brands do what they can. Nearly one-quarter applied to online lenders. Many lean on cards too. An NBER summary found 80% of firms used corporate credit cards. After rate hikes, interest payments jumped 60%. I understand why people reach for flexibility. I just do not think a credit card is a capital strategy for a scaling brand.

Give Junior Debt a Precise Job

Bridge a Timing Gap

I want junior debt to solve a specific problem. Supplier deposits. Inventory ahead of a launch. Marketplace payout delays. Wholesale receivables. Seasonal working capital. That is the level of clarity I am looking for.

If the answer is "general cushion," I keep pushing. Cushion sounds good in a board meeting. It gets expensive in the bank account.

One CPG brand we worked with had strong repeat customers, healthy margins, and steady month-over-month growth. Demand was there. The problem was timing. They had to pay suppliers 60 days before receiving inventory, and then wait again for platforms like Amazon to release payouts. Traditional lenders looked at that and saw volatility. I saw momentum and a cash gap.

This is where a lot of stacks get messy. Other providers wanted to underwrite that business one channel at a time. One offer for Amazon. Another for Shopify. A different product for wholesale. Suddenly the CFO was dealing with three or four repayment schedules. That is more noise, not more control. If you need multiple lenders to finance one business, something is off.

Make Sure the Senior Lender Is Comfortable

If you already have a senior lender, slow down before you add another layer. Ask the obvious questions first. What exact gap is the junior debt bridging? How much cash is truly needed? What does the new payment structure do to monthly liquidity? And is the senior lender comfortable with another capital provider in the stack?

This matters because many senior lenders still use covenants that do not fit ecommerce. I have seen inventory-on-hand requirements treated like a safety feature because the bank sees inventory as collateral. For the brand, that same inventory can be expensive. It ties up cash. It adds storage fees. It can force markdowns if the season moves on.

So before you layer in junior debt, define the gap with precision. Then model how the new capital changes cash flow. Then get alignment with the senior lender. Terms are the keys.

Match Each Layer of Capital to the Right Use

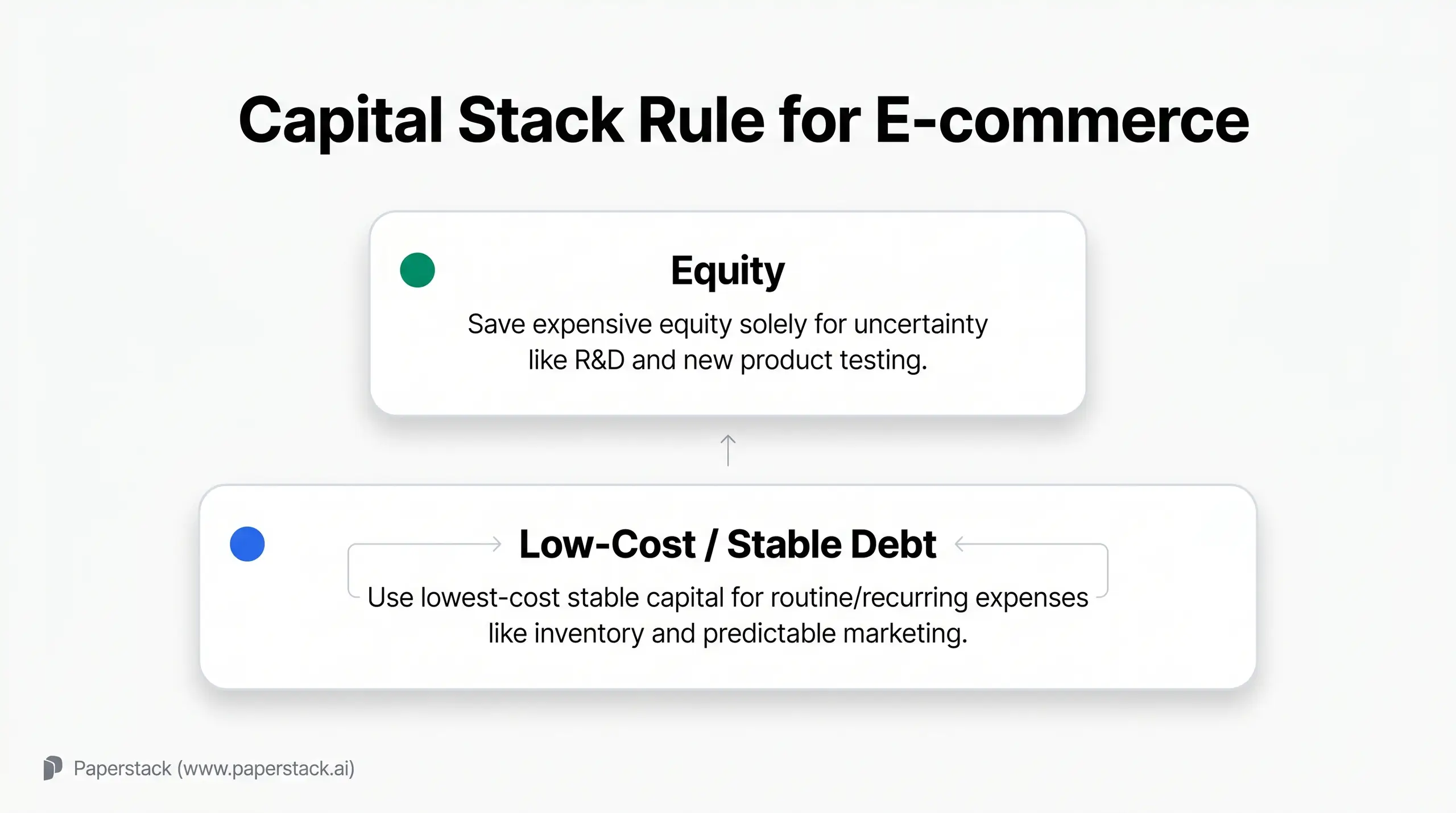

I like a simple rule. Use your lowest-cost, most stable capital for the most stable part of the business. Use flexible non-dilutive capital for recurring expenses with a clear payback. Use equity for uncertainty.

I feel strongly about this because I have seen too many brands use equity for routine inventory or predictable advertising. The most expensive capital that you can use for inventory or predictable marketing is equity. Save equity for R&D, new product launches, and experiments where ROI is still unclear.

There are exceptions. If you are very early, have no credit history, and are still testing market fit, equity may fund that first inventory order. I understand that. But once the business has a track record, recurring working capital should be matched with more efficient capital.

Marketing is where this conversation usually gets tense. Traditional lenders often see it as burn. In growing ecommerce brands, that misses the point. Marketing is often one of the top three expense lines. I have seen brands allocate 15% to 25% of annual revenue to it. If that spend has a long record of producing profitable sales, you should treat it seriously and defend it with numbers.

That means showing how long the brand has been doing it. One month is very different from one year. One year is very different from five. I want to see historical ROAS, contribution margin after all costs, and whether the model depends on first-purchase profitability or long-term LTV. I also want CFOs talking directly with the marketing team. You need to know the efficiency curve as spend scales. You need to know the minimum ROAS that still leaves room for profit.

And sometimes the right answer is to spend less, not more. At certain stages, I would rather see a brand focus on upselling existing customers, increasing AOV, and lifting LTV through email and product drops. More capital should make decision-making sharper. It should not push the team into lazy spending.

Stop Paying for Money You Are Not Using

The Cost of False Comfort

A lot of CFOs sleep better when a big unused loan is sitting in the bank. I understand the instinct. Liquidity feels safe. But comfort has a price.

The question I always come back to is simple: what do you do with the cash, and if you do nothing, how much does it cost your business to keep it in the bank account? If the money is not being deployed right away, you are still carrying the cost of that capital. That drag hits margin quietly. Then one day it shows up everywhere.

I compare it to maxing out a credit card personally because it makes you feel prepared. The money is there, but now the balance is working against you from day one.

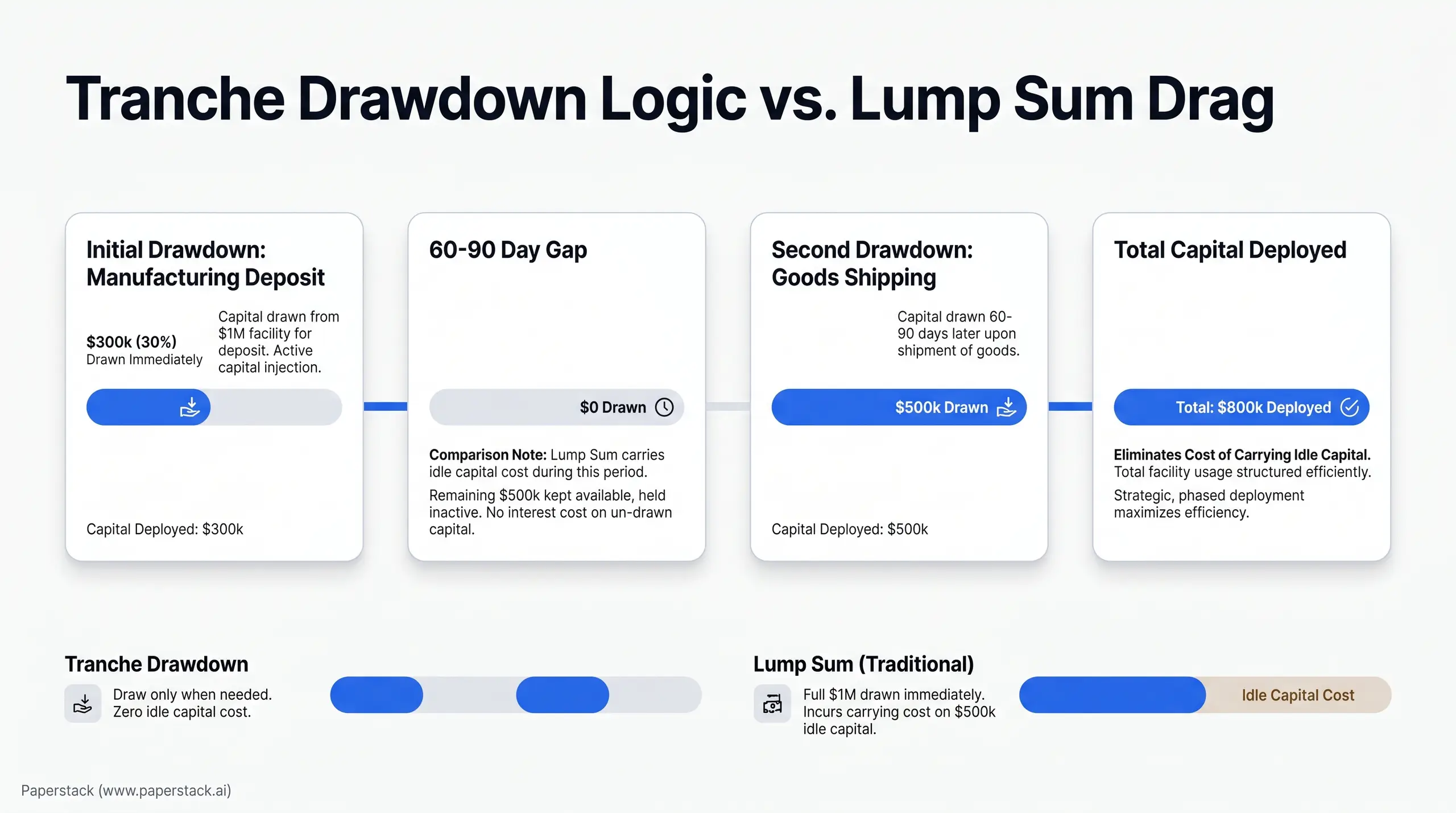

I worked with an apparel brand doing around $10 million in revenue that had fallen into exactly that trap. They had a lump-sum loan and were remitting 17% of daily cash flow against capital they did not need all at once. We helped restructure that into a commitment of more than $1 million, with $300,000 drawn immediately and another $500,000 available 60 to 90 days later. They kept the access. They removed the cost of carrying idle capital. That is real margin protection.

Draw in Tranches

I strongly prefer committed capacity with planned draws over one big advance. Ecommerce cash needs show up in stages. A 30% manufacturing deposit today. The balance when goods leave the factory. Freight after that. Then the marketing push once inventory is close to landing.

So structure your capital the same way. If the manufacturer needs 30% now, draw 30% now. Wait to draw the rest until the goods ship. Do not pay for capital during a 30- to 90-day production window if the money is just sitting there.

The only time I like a large upfront draw is when the cash is immediately creating value. Maybe you are securing a bulk raw-material discount. Maybe you are paying AP early to get a discount. Maybe you are funding highly profitable sales right away. Fine. But if the cash has no immediate job, I would not pull it down just because it is available.

That thinking shaped how we built Paperstack. I did not want the small one-off advance model. I wanted a facility that gives a brand room to move, with draws as needed and remittance caps so growth does not punish liquidity. Just because your business qualifies for a million dollars doesn't mean you have to take it all.

Treat the Business as One Cash Flow Engine

A lot of brands look stable in reality and chaotic on paper because their capital stack is fragmented. One provider advances against Shopify. Another looks at Amazon. Another factors wholesale orders. From the outside, it might look like a riskier business than it is in reality when a business has several capital providers instead of one.

I saw this with a multichannel brand whose revenue came from Amazon, Shopify, and wholesale. Each provider wanted to underwrite only one piece of the business. The result was three or four lenders and three or four repayment schedules. That does not help a CFO forecast cash. It makes the business harder to read, especially during seasonal swings.

On paper, many offers look similar. The structure behind non-dilutive capital is where the real difference shows up. I would look past the headline rate immediately. What is the actual total cost of capital once you include origination fees, wire fees, underwriting fees, and admin charges? Hidden fees change the economics fast.

Then I would look closely at remittance. Is there a minimum payment that becomes painful in a slow month? Is there a cap that protects liquidity in a strong month? I like capped structures because fast-growing brands should not be drained just because they had a big revenue week. We do not need to penalize growth.

I also want to know what revenue the provider is really counting. If Shopify is only 30% of your business, a lender that looks only at Shopify is missing most of the picture. Ask how wholesale is treated too. Does the lender count revenue when a draft order is created, or when cash actually lands in the bank? That detail matters a lot more than people think.

Then ask about control. Do funds go to your designated bank account, or does the lender pay suppliers and platforms on your behalf? And who supports you after closing? I prefer relationship continuity. A capital partner should not disappear the moment money is deployed.

Selling Out Hurts More Than People Admit

I say this often because it still gets framed the wrong way. Selling out is a financial failure or operational failure more often than people want to admit. From the outside, it might look like a celebration, but from the inside, it's a massive pressure internally operationally for the team.

I watched a wellness brand around $5 million in revenue go viral and sell out on Amazon. The short-term spike looked exciting. The aftermath was painful. Their Amazon search ranking dropped. Visibility became harder to regain. The team lost momentum and had to spend again to rebuild what they already had.

I have seen the same thing during the holidays. A viral moment empties inventory right when the brand has paid the most to acquire attention. Then trust breaks. CAC rises because you have to re-engage disappointed customers later. Fixed costs like warehouse rent keep running even when there is no inventory to sell. And if the team rushes a restock, unit economics get hit again through emergency air shipping or smaller production runs.

There is also an internal cost that does not show up quickly enough in the model. Your marketing team has to shut down campaigns that were finally working. That is frustrating. They fought hard to build that momentum, and now the company has to work twice as hard to get back where it was.

This is why I push CFOs to challenge the standard playbook around peak periods. Around Black Friday, CAC can rise so fast that the sale stops being attractive. I would rather see you calculate whether that higher CAC still leaves room for profit. I also like starting holiday campaigns earlier. Capture customers before the rush. Protect your CAC. Protect your inventory. Protect your margin.

Use Discipline When Volatility Hits

My leadership philosophy is unapologetic optimism. For me, that is not blind positivity. It is discipline. You plan for volatility so the business has options when the shock shows up.

One brand partner was hit by new import tariffs that pushed landed costs up almost overnight. A lot of teams would have frozen inventory orders and cut marketing immediately. We took a different route. We ran conservative, most likely, and optimistic scenarios. We modeled what happened if tariffs held, dropped, or expanded. We looked at unit economics, whether costs could be shared with suppliers, and what customer retention might look like if pricing had to move.

That process gave the team enough confidence to keep ordering at scale and protect supplier relationships while competitors hesitated. When the market stabilized, they were one of the few brands still fully stocked and they captured market share.

The same discipline matters when the shock is operational. If a port strike or manufacturing delay cuts incoming inventory, I would reduce marketing spend and promotional pressure. Stretch the inventory you still have. Preserve the margin you will need for the emergency costs that usually follow. Growth isn't just about how much you sell, it's about when you sell it.

Sometimes the Best Capital Move Is a New Revenue Stream

Debt is one lever. Revenue mix is another.

I think about a snack brand around $10 million in revenue that was very strong in Q4 and much tighter in the summer. In that kind of business, a fixed payment structure in the slow season creates pressure at exactly the wrong time. A revenue-based structure can help because repayments move with the business. But I would also look at whether the brand can diversify revenue and smooth the curve.

This is where B2B can strengthen a DTC business. I have seen brands sell in bulk to banks and law firms for corporate gifting. That creates bigger order sizes, different seasonality, and often higher lifetime value. It can also work as funded sampling. The corporate buyer pays for the product, and the recipients may later convert into direct customers. I think of that as acquiring customers at someone else's cost.

There is a cash flow angle here too. If the order includes personalization, like a company logo, you have a stronger case for asking for an upfront security deposit because the buyer understands that customized inventory cannot easily be resold. And once one office says yes, you can use that win to get introductions to other branches. I like that land-and-expand motion because it gives the brand more control over revenue instead of relying only on ad performance.

How I Pressure-Test the Stack

Before I say yes to a junior layer, I run the same sequence every time. First, I want the exact use of funds. Supplier deposit, proven marketing, inventory build, payout gap, or something else. Then I want the math. Show me the business over 12, 24, or 36 months. Show me how a specific capital injection turns into top-line revenue and cash generation. Back it with the data. Show it with the numbers.

After that, I move to downside planning. What happens if the slower month shows up first? What happens if inventory lands late, ROAS slips, or tariffs move again? If the structure only works in the optimistic case, it is too tight. I also want the real all-in cost, including fees, remittance mechanics, and whether the business can comfortably handle that structure in slower periods.

Then I look at fit. Is the senior lender comfortable? Are all channels being counted? Does the provider understand the timing of wholesale and marketplace cash? If the product is venture debt, timing matters too. It often shows up right after an equity raise, but I still want the warrants modeled over two to ten years so the true cost of capital is clear before anyone signs.

And finally, I look at the relationship. If the capital partner disappears after closing, that is a warning sign for me. In ecommerce, the operating environment changes quickly. Your capital partner should be able to keep up with that reality.

Final Thought

The best capital stack fits your business.

It fits your seasonality, your inventory cycle, your marketing engine, and your payout timing. It gives you room to move without paying for idle cash, breaking your margins, or forcing frantic decisions when the market shifts. That is the standard I push for. When you build the stack that way, capital starts working with your business, grows in rhythm with your brand, and gives you more confidence in every decision that follows.

Frequently Asked Questions

How do we structure intercreditor agreements when layering junior debt behind a senior bank revolver?

You must formally subordinate the junior debt. I look for intercreditor agreements that clearly define payment blockages and secondary collateral rights. If the senior lender views your inventory as their collateral, the junior facility must remain strictly unsecured or properly subordinated to avoid triggering technical defaults on your primary covenants.

Does adding junior debt to the capital stack lower our overall Weighted Average Cost of Capital (WACC)?

Yes, especially if it replaces equity for routine working capital. While junior debt carries higher rates than senior bank loans, it remains significantly cheaper and non-dilutive compared to equity capital. I view this as a disciplined margin-protection strategy to fund predictable marketing or inventory without sacrificing your long-term ownership stake.

Should we use junior debt to refinance existing corporate credit card balances?

Absolutely. Relying on maxed-out cards is dangerous for scaling brands. With small business credit card interest payments jumping 60% recently, according to NBER research, refinancing that volatile, high-interest balance into a clearly structured junior debt facility instantly restores liquidity, protects margin, and stabilizes your entire cash flow engine.

What are the statistical odds of securing junior debt from alternative lenders versus traditional banks?

The approval gap is substantial. If you approach a large legacy bank, approval rates sit around 58%. However, alternative online lenders approve roughly 82% of financing applications, according to Federal Reserve analysis. Alternative lenders actually underwrite ecommerce metrics like historical ROAS and marketplace payouts, rather than just demanding hard assets.

How does a revenue-based junior debt facility impact our Debt Service Coverage Ratio (DSCR) during slow seasons?

A properly structured revenue-based junior facility actually protects your DSCR. Because remittances automatically scale down when daily sales drop, your fixed debt burden shrinks during seasonal lulls. I always look for structures with remittance caps to ensure you aren't drained during revenue spikes, keeping working capital utilization highly disciplined year-round.