If you lead finance at an ecommerce brand, you know this feeling well. Revenue is growing. Demand is there. The business looks healthy in the board deck. Still cash still feels tight.

When I see that, I do not start with the P&L. I start with the capital stack. In ecommerce, cash pressure usually comes from structure. Money leaves on one schedule, comes back on another, and debt service adds a third clock on top of both.

I learned this in banking. I kept seeing systemic lending gaps

I saw a brand thing around the $5 million revenue mark. Brands that needed real working capital often could not get a commercial facility that fit how they operated. They were pushed toward personal lines of credit that were too small and too rigid.

Axios recently described cash flow as the oxygen of every business. I agree with that. In ecommerce, timing decides whether that oxygen reaches the business when it matters. Once timing breaks, things can get painful fast. Across the market, a rising share of small businesses are missing payroll when cash gets tight. No CFO wants to get anywhere near that point.

A refinance should give you breathing room. It should also sharpen the business. Here are the five steps I would take.

1. Start with Timing, Not Rate

Map Where Cash Gets Stuck

When a CFO asks me about refinancing, I want to see timing before I talk about price. Your cash conversion cycle is a simple place to start. You already know the formula. Days inventory plus days receivable minus days payable. What matters is the gap it reveals.

Tracking that cycle helps expose where cash gets stuck. In ecommerce, I want to see supplier deposits, final inventory payments, production lead times, freight timing, Amazon payout delays, wholesale collections, ad spend, expected payback windows, and every lender remittance on one page. Even a healthy pipeline can still mask sluggish liquidity when cash out runs ahead of cash in.

I care a lot about cash flow quality. For me, that means predictability, timing, and sustainability. A refinance built around those three things will hold up much better than one built around collateral alone.

Refinance the Real Gap

One CPG brand we worked with had strong repeat customers, good margins, and steady month-over-month growth. Their problem was not demand. They had to pay suppliers well before inventory landed, and then wait for Amazon and other channels to release cash. Traditional banks read that as volatility. I read it as a timing gap.

That difference matters. If you refinance before you map the real gap, you can replace one bad structure with another. I want to know whether the strain is coming from inventory timing, ad spend payback, wholesale AR, or debt service itself.

Bring marketing into this discussion early. For many growth brands, marketing can run 15% to 25% of annual revenue. That makes it one of the biggest expense lines in the business. If you want a lender to understand that spend, show the ROAS history and the payback period. Back it with the data. Show it with the numbers.

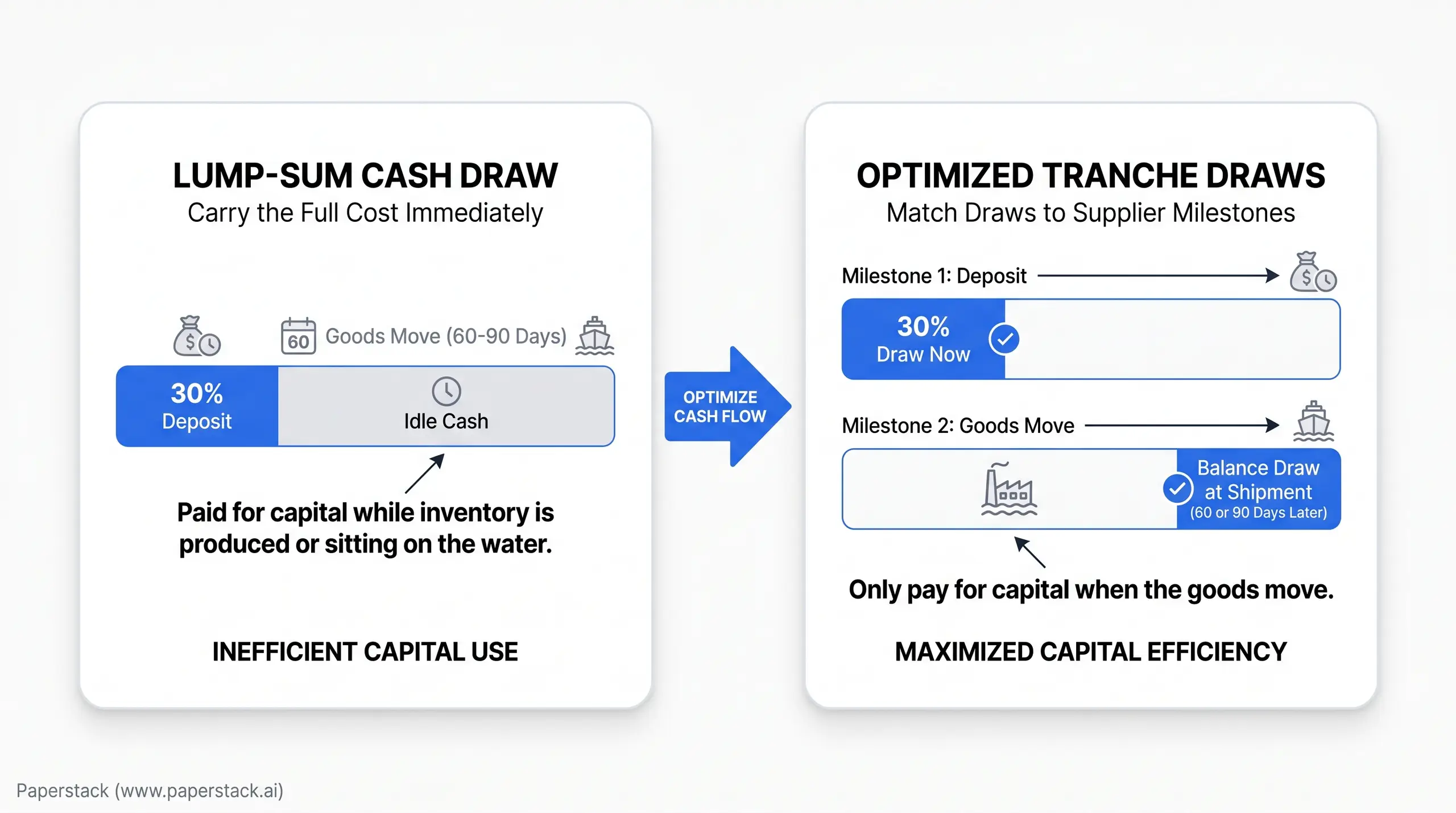

2. Cut the Lump Sum Down to What You Will Actually Use

Stop Carrying the Cost of Idle Cash

This is one of the most common refinancing problems I see. A brand gets approved for a big number. The team feels safer taking the full amount upfront and leaving it in the bank. I understand the instinct. A large balance can feel like control.

Then the remittance starts. Suddenly 17%, 20%, sometimes 25% of daily cash flow is leaving the business to service capital that is still sitting idle. I often compare this to maxing out a credit card personally because the limit is there. The sense of security is real. The cost is real too.

I remember an apparel brand that had taken a larger upfront facility and was remitting close to 25% of daily sales. It became especially painful during the low season. Their fixed costs stayed fixed, but a quarter of incoming sales was still going out the door. The business was carrying the cost of that capital without getting the benefit of it.

We went back to basics. We looked at what they actually needed, when they needed it, and how much the business could comfortably service in weaker months. Then we restructured the facility into draws every 60 days and refinanced the remaining balance over a longer payback period. That gave the brand more cash in the bank at the end of the day and much less pressure on margins.

Match Draws to Supplier Milestones

My rule is simple. If you will not be using the capital in the next 30 to 45 days, leave it undrawn.

This matters even more when inventory is involved. If your manufacturer needs a 30% deposit now and the balance when goods ship 60 or 90 days later, draw the 30% now. Take the rest when the goods move. There is no reason to pay for capital while inventory is still being produced or sitting on the water.

That is why I prefer revolving facilities that let brands draw in tranches as they need capital. At Paperstack, we built around that logic. A refinance should lower pressure, not create new pressure from money that is doing nothing in the bank account. Every CFO should ask one blunt question: what do you do with the cash, and if you do nothing, how much does it cost your business to keep it there?

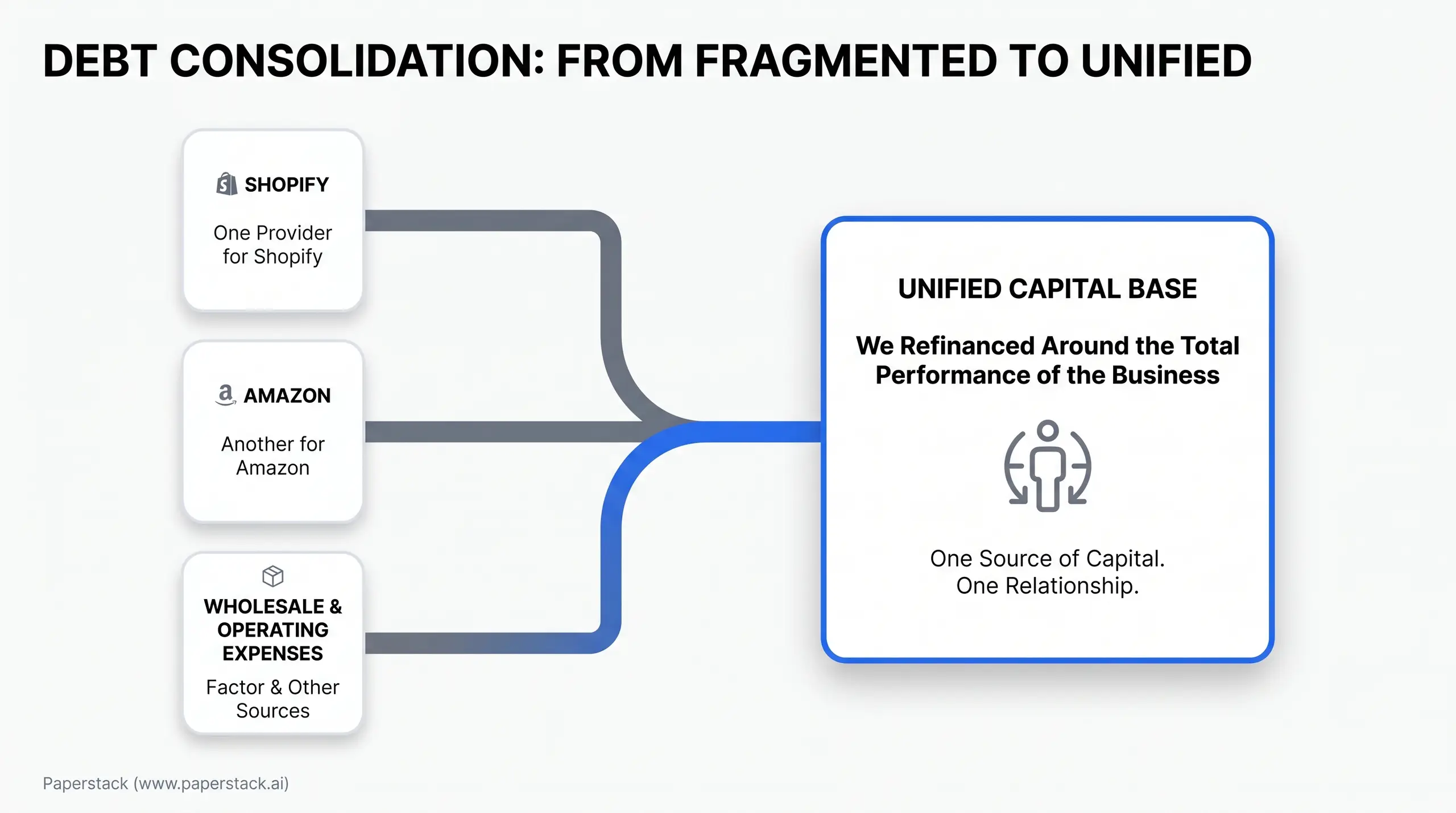

3. Refinance the Whole Business, Not One Sales Channel

Fragmented Debt Creates Hidden Risk

A lot of medium-sized brands build their capital stack one piece at a time. They take one provider for Shopify, another for Amazon, maybe a factor for wholesale, and something else for operating expenses. From the outside, that can look diversified. Inside the business, it creates blind spots.

Each lender is underwriting a specific channel and not the whole business together. If Shopify is only 30% of your revenue, a provider looking only at Shopify is missing 70% of the story. The bigger problem shows up when one channel slows. If an Amazon lender gets spooked by a temporary dip and calls the balance, that can put additional stress on cash flow and trigger a domino effect across the rest of the stack.

The CFO also pays a heavy operational price. You are managing multiple reporting requests, multiple repayment schedules, and multiple maturity dates. That is time you should be spending on planning, margin protection, and growth.

Consolidation Gives You a Cleaner Operating Base

We saw this with a CPG brand selling across Amazon, Shopify, and wholesale. Other capital providers wanted to underwrite only one channel at a time. That left the team juggling three or four lenders, each with different rules. Their real business was stronger than any one channel view suggested.

We refinanced around the total performance of the business. One source of capital. One relationship. One clearer view of repayments. That gave the team room to say yes to strategic retail partnerships without starving the DTC channel or cutting marketing just to preserve cash.

I still want CFOs to think about concentration risk. A single provider can tighten terms too, and refinancing out of that situation takes time. So ask the hard questions upfront. Ask who stays on the account after closing. Ask how they react when one channel slows and another grows. The best capital partners act like collaborators. The relationship should not end once the funds are deployed.

For wholesale-heavy or Amazon-heavy businesses, I usually prefer remittance tied to bank deposits because it tracks when cash actually lands. In my experience, one partner who understands the full business gives you a much stronger base for forecasting than three or four lenders pulling in different directions.

4. Renegotiate the Structure Before You Chase the Rate

Terms Are the Keys

A lot of offers look similar on the surface. The headline price may look clean. The word non-dilutive is on the page. The pitch sounds fast and founder-friendly. Then the mechanics show up.

This is where I slow down. Terms are the keys.

I start with the true total cost of capital after every fee. That means origination, underwriting, admin, wires, and even simple charges for changing a bank account. Then I look at remittance in a slow month and in a big month. Is there a minimum payment that will hurt when sales soften? Is there a monthly cap that protects liquidity if the brand grows fast? You do not want to pay a full month's remittance in the first week because the structure was too aggressive.

I also ask how wholesale revenue is treated. Does the lender count a draft order in Shopify, or only the cash that actually lands in the bank account? That detail changes forecasting. I ask where the money goes too. Does it arrive in your operating account, or does the provider pay suppliers or ad platforms directly? Control over deployment affects how quickly you can respond when the business changes.

At Paperstack, we built remittance caps very intentionally because I never wanted a brand to be penalized for growth. If a business is scaling fast, the capital should support that momentum instead of draining liquidity out of it.

Bring the Data That Tells Your Story

Traditional banks still miss a lot of this. I saw it clearly with the beverage brand from my banking days. Healthy margins and steady cash flow were not enough because the underwriting model was not specifically built for CPG brands. Hard assets mattered more. Marketing was treated like burn. Seasonal inventory turns were treated like risk.

I also still see traditional facilities come with personal guarantees, slow in-person processes, and inventory-on-hand covenants that work against how ecommerce brands actually operate. A bank may want more inventory sitting still because they view it as collateral. For the brand, that can mean storage costs, slower turns, and discounting later just to free up cash.

If you are refinancing out of those structures, tell the story to the next lender and back it with historical performance. Show your lowest and highest inventory levels by month. Show the natural seasonality. Show how quickly inventory turns when launches work. Show two, five, or even 10 years of marketing data if you have it, so ROAS is understood as a real budget discipline and not a random experiment.

If venture debt is part of the conversation, model the warrants early. The stated coupon is only one piece of the true cost of capital. A refinance should give you cleaner cash flow, cleaner forecasting, and more control. A lower headline rate alone does not guarantee any of that.

5. Turn the Refinance Into a Better Operating Rhythm

Match the Capital to the Expense

A refinance should do more than relieve pressure this quarter. I want it to improve how you fund the business going forward.

I feel strongly about this part. Equity capital is used for R&D, new products, and channels where the return is still uncertain. The most expensive capital you can use for inventory or predictable marketing is equity. Those recurring expenses should be funded with non-dilutive capital when the math is clear.

That means finance and marketing have to work from the same model. You need to know whether the business needs profitability on the first order today or whether LTV carries the model. You need to know your minimum acceptable ROAS as spend scales, because efficiency usually degrades as budgets get larger. Some brands can still be profitable at 2x or 2.5x ROAS. Others cannot. Your lender should understand that math too if marketing is part of the plan.

At certain stages, the smarter move is to pull back on acquisition and push AOV and LTV with the customers you already have. A new drop to your email list can do more for cash flow than another expensive push for cold traffic. I also challenge the automatic habit of increasing ad spend during peak periods. Around Black Friday, CAC can spike hard. Starting campaigns earlier often gives you cleaner CAC and smoother inventory depletion.

Plan for Volatility Before the Market Forces You To

I have said this many times because it matters: selling out is a financial failure or an operational failure. I have seen a wellness brand go viral on Amazon and sell out. From the outside, it looked like a win. Inside the business, it hurt. Search ranking dropped. Visibility got harder to recover. The team had to rebuild the relationship with the customer and work twice as hard to get back where they were.

Stockouts create pressure everywhere. Marketing has to stop campaigns that were working. Loyal customers hit a dead end. Fixed costs like warehouse rent keep running. Then the finance team may be forced into expensive air freight or smaller production batches that damage unit economics.

When volatility hits, I go straight to scenario planning. One of our brand partners got hit by new import tariffs that raised landed costs almost overnight. We modeled conservative, most likely, and optimistic cases. We looked at unit economics, pricing flexibility, supplier negotiations, and retention risk. That discipline gave them options. They kept ordering, maintained supplier relationships, and were in stock when competitors hesitated.

Sometimes the right move is to intentionally reduce marketing and discounting for a period, especially when supply chain delays hit. Stretch the inventory you have. Protect margins. Restart demand when supply catches up.

And if your DTC business is too dependent on one season, use the refinance to deliberately diversify revenue. I have shared before how some brands sold products in bulk to banks and law firms for corporate gifting. With personalization, they could justify upfront security deposits because customized inventory could not be resold easily. Those orders created larger quantities, steadier revenue, and exposure to new consumers. When gift recipients later converted into DTC buyers, the brand was acquiring customers at someone else's cost. I like B2B for another reason too. It gives the team more control because revenue comes from outbound work, not only ad performance. For a CFO, that is a structural improvement to cash flow quality.

Final Thought

When I look at ecommerce refinancing, I keep coming back to one idea. Free cash flow comes from fit. Your capital structure has to fit the real timing of your business.

Start by mapping where cash gets stuck. Cut down oversized draws and move to tranches. Refinance around the whole business instead of separate channels. Negotiate the mechanics with as much care as the rate. Then use the new structure to support better inventory planning, smarter marketing, and real scenario planning.

I built Paperstack because I believed modern commerce brands needed a better capital foundation. I still believe that. When the structure is right, you create more breathing room. And to me, that is what unapologetic optimism means in finance. You plan hard. You stay adaptable. You give the business room to grow.

Frequently Asked Questions

How does refinancing repair a strained Cash Conversion Cycle?

Refinancing attacks where capital gets trapped. The CCC measures time "to transform inventory and services into cash on hand" (Axios). A structured facility bridges the gap between supplier deposits and final channel payouts, providing breathing room without draining your operating accounts.

Can flexible refinancing prevent critical operational failures during seasonal sales troughs?

Yes. A rising share of businesses are "missing payroll" (Axios) when cash gets tight. Refinancing ecommerce operations with tranched debt ensures fixed repayment structures do not cannibalize baseline liquidity, protecting essential outflows like payroll during predictably slow seasonal periods.

Why is a unified financial calendar critical before initiating an ecommerce refinance?

A strong pipeline "can still mask sluggish liquidity" if payables precede inflows (Axios). Mapping marketing, inventory, and debt schedules on one calendar exposes your true structural deficit, ensuring you borrow exactly what is needed rather than over-leveraging based solely on top-line revenue.

How should a CFO weigh debt refinancing against raising additional equity?

Equity is your most expensive capital, best reserved for R&D. For predictable inventory and marketing, I recommend non-dilutive debt. Refinancing ecommerce debt correctly provides the working capital required to scale proven acquisition models without unnecessarily sacrificing board seats or valuation upside.

What internal risks threaten liquidity even after securing a highly flexible refinance?

Poor financial literacy is a major blind spot. 50% of small-business owners admit to ongoing fiscal challenges (Axios). Even with great refinancing, if your teams lack the discipline to accurately forecast minimum ROAS and inventory turns, any capital structure will ultimately fail.